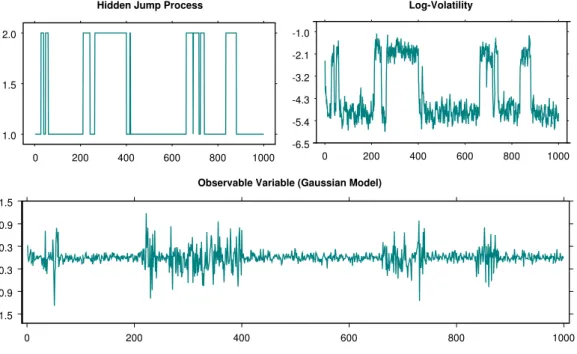

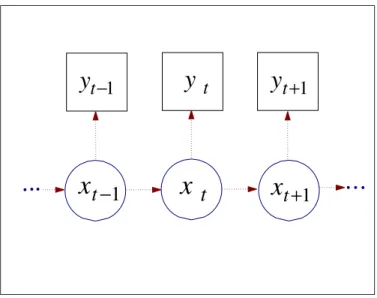

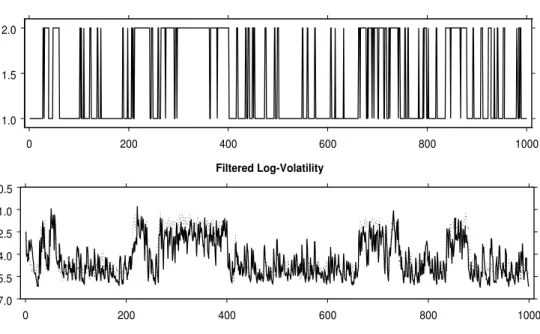

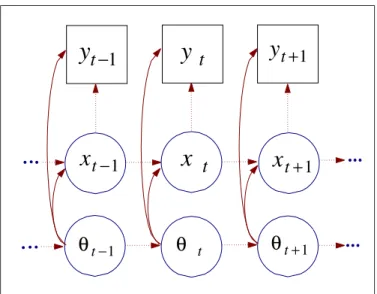

Bayesian Inference for Generalised Markov Switching Stochastic Volatility Models

Texte intégral

Figure

Documents relatifs

Time evolution of proteolysis index has been measured and modelled on five different types of pork muscle under different accurate temperature and water activity

Inspired by the Bayesian evidence framework proposed in [31] to solve noisy interpolation problems, we have derived a generic and reliable hierarchical model for robust

The effect is particularly important in small samples (or in large samples with small but clearly distinct clusters) because, in the basic non-parametric bootstrap on a small

Figure 3 Colorectal cancer screening (CSS) attendance rates according to deprivation scores (quintiles), and the degree of urbanisation (urban, rural, all IRIS) (solid lines:

The Hamiltonian Monte Carlo algorithm and a method based on a system of dynamical stochastic differential equations were considered and applied to a simplified pyrolysis model to

When used in conjunction with MS-CHAP-2 authentication, the initial MPPE session keys are derived from the peer’s Windows NT password.. The first step is to obfuscate the

In Laboratory I the group are expected to prepare a work plan or a census calendar for one of the participants' country.. Then, based on the work plan the group will proceed and

This paper investigates the contribution of fundamentals to the persistence of currency crises by identifying the determinants of high volatility in the exchange market pressure index