Individual Private Pension Insurances: the effects of

socio-demographics characteristics on poverty

Najat El Mekkaoui de Freitas1, Gordon Clark2, Bérangère Legendre3

Preliminary version

December 2009

Abstract

Funded private pillars are well developed in many countries such as the United States, the United Kingdom, Canada, Switzerland and the Netherlands. In France, the development of occupational pension plans has been limited. However, in this country, households tend to increase their personal saving by contracting life insurances in order to finance their retirement. By encouraging the individualization of retirement planning, reforms of public pension systems could expose a vulnerable part of the population to the risk of poverty. Among households, low-income and women are particularly vulnerable during their working life and then during their retirement period. In France and in other OECD countries, the trend to have more individualized pension raises the question of the poverty during the retirement period.

In this context, could life insurances and private pension contracts avoid the risk of poverty? In this paper, we analyze the behaviour of life insurance holding in France, by using an econometric model and studying statistically the risk of poverty among Retired.

KEYWORDS: PRIVATE PENSION INSURANCE, AGEING, POVERTY

JEL classification: C10, I32, J26, G22.

1

LEDa, Chaire Dauphine-Ensae-Groupama, Université Paris-Dauphine et Oxford University.

Email : [email protected], adress : Office : A520, place du Maréchal de Lattre de Tassigny – 75016 PARIS.

2 Oxford University. 3

Introduction

The combined pressures of increased lifespan and reduced fertility are driving public pension systems towards reforms. On one hand, less generosity in terms of benefits is being viewed as a means of safeguarding the systems’ sustainability, by avoiding a strong disequilibrium between receipts and expenses. On the other hand, additional private saving is being recommended in order to maintain an appropriate standard of living throughout the entirety of the life cycle. According to an OCDE study, an increased level retirement saving is urgently needed, particularly in countries where pay-as-you-go benefits are due to decrease (Börsch-Supan, 2005).

In Europe, by introducing favourable fiscal dispositions, these recent reforms tend to encourage people to contract private pensions, or more generally to save more in order to prepare the retirement. In France, this process is particularly recent. The reform of 2003 introduced individual and professional pension plans4. However, French households prefer making long-term investment that will provide a source of retirement income by contracting life insurances.

By encouraging the individualization of retirement planning, reforms of public pension systems could expose a vulnerable part of the population to the risk of poverty. Among households, low-income and women are particularly vulnerable during their working life and then during their retirement period.

The poverty rate for seniors aged 65 was 19% in 2007 in the European Union, and 13% in France (Eurostat). It includes the share of persons with disposable income below the poverty threshold, set at 60 % of the national median disposable income. In France, according to the national statistical office (INSEE), the poverty rate5 today of single person aged 65 and more is 15.5% compared to 7.3% for people belonging to household.

This paper focuses on the role that insurance annuities can play to avoid poverty among older households in helping them to manage retirement wealth. Such a correlation between poverty at retirement and life insurance holding has not been analyzed extensively.

The annuities considered in this paper are private, life, pension annuities - i.e. financial contracts that provide a monthly or annual sum to an individual in retirement as long as they live. Life insurance contracts in France are mostly endowment contracts.

This paper is divided in five sections. In the second section, we present a brief literature review on poverty during the retirement and the holding of life insurance. The third part presents the survey and data used. Then we expose in the fourth part some facts about poverty and private pension holding in France, before presenting an econometrical model. This fifth part allows us to determine if reduction of the risk poverty and life insurance holding are observed. Lastly, we conclude.

1. Literature review

Because of the longevity risk and pension reforms, many households need to save during their active life. Many papers conclude that social protection systems decrease the probability of poverty after retirement. But the recent demographic and economic constraints, conducting to reforms of pension system in France and in other countries, could impact the level of poverty among old people. Consequently, in the future, private saving could allow people to avoid being poor after retirement.

Pure endowment insurance contracts are often identified as pure saving contracts, and have not led to specific studies. Moreover, the characteristics of life insurance contracts and the amounts invested in these contracts vary from country to country, due to the institutional features (taxation) of the social welfare system.

Life insurance demand entails many motives, some shared by all savings products, others being more specific. The certainty-equivalence model underlines three motives, the life-cycle, the intertemporal substitution, and the bequest motives (see Browning and Lusardi, 1996). However, as the certainty-equivalent model assumes a quadratic utility function, it cannot capture the precautionary motive. This is the reason why the “standard additive model” emerged since it allows for an adequate treatment of uncertainty, particularly of uncertainty of future incomes (Caroll, 1992, Irvine and Wang, 2001). The existence of liquidity constraints strengthens the need for precautionary saving (Deaton, 1991).

Household demographics also influence the precautionary saving behaviour (Attanasio and Weber, 1995, Bernheim and al., 1999). The standard additive model, augmented with demographic variables thus offers a more exhaustive explanation of life-cycle savings. Tax exemptions and a retirement motive (due to the fragile financial soundness of the French pay-as-you-go public pension system) constitute other motives for private pension insurance demand. Kimball (1992) shows, the “cautious” individual will adopt protectionist behaviour to attenuate the risks confronting his/her life and health, so that the demand for insurance will increase. However, this behaviour might also reflect a wish to make inheritances.

Using the French survey Patrimoine of 1998, Bernard, El Mekkaoui de Freitas, Lavigne and Mahieu (2002) show how the demographic structure and the age impact the holding of life insurance or private voluntary pension contracts. Households aged of 50 and more hold more

contracts than younger households. Whereas complementary pension contracts holding tend to decrease after the age of 60, it is not the case for life insurance contracts.

Using the same survey, Arrondel and al. analyzed socio-economic determinant of life insurance holding in France. Households with children tend to buy more insurance in order to prepare their retirement, whereas households without children preferred life insurance in case of death in order to protect their family.

The risk of poverty in Europe has been extensively analysed in the literature. Using the European Household Panel, Cohen S. and Lelièvre M. (2002) conclude that the European retirees benefit from the same standard of life than active people. However, there are disparities among the population of Retired. They identify many factors impacting the risk of monetary poverty: the composition of the household, the sex, the activity rate, the sources of income. In Portugal the risk of poverty is high among the retired population as the pension system is more recent than in other countries. At the end of the 90’s, half the lonely retirees were under the threshold of poverty. Private and public pension represented less than 50% of the income in household with at least one pensioner. Incomes from activity represented 44% of the household’s income. The retired women, living alone, suffered particularly from the poverty.

Many papers (Drouhin, 2002, Hachon, 2007, Whitehouse & Zaidi, 2008) point out the fact that inequalities of life expectancy have an impact on the living standard during the retirement period. Whitehouse and Zaidi (2008) concluded that this phenomenon is more important among men. By studying different areas of economic policy and using data from Germany, the United States and the United Kingdom, they conclude that inequalities of mortality reduce the progressivity of public pension systems. According to Brown (2002), it involves a regressive redistribution.

2. Survey method and implementations

The most comprehensive and recent information on French households’ behaviour is provided by the Patrimoine Surveys, which was conducted by National Institute of Statistics and Economic Studies -Institut National de la Statistique et des Etudes Economiques (INSEE) in 2003-2004 on the metropolitan territory, among 9 692 households.

2.1. The Patrimoine Survey

The Patrimoine 2004 Survey, including 9 692 households, was completed by the INSEE between October 2003 and January 2004 on the entire metropolitan area.

The survey is composed of four tables. The first is named ‘Individuals’ covering 22 821 individuals (48% men and 52% women) aged 0 to 99 years old. All of these individuals are part of a household which then constitutes the second table ‘Households’ carried out on 9 692 households. The third table ‘Product’ informs us of the savings and financial products as well as the capital holdings of the household. Finally, the last table ‘Transmission’ refers to the different transfers of capital between ancestors and descendants.

This survey particularly informs on the financial and non-financial assets of the household belonging to the selected individual questioned, their income, their age, their social-professional category, their education/training, their marital situation, and their status (active, inactive, retired). Furthermore, the survey also includes the type of asset detention retained by the household (checking account, savings account, real estate, life insurance, corporate savings, etc.). Retirement pensions, both state and private (type and amount), are also presented.

The Patrimoine 2004 Survey also provides data on voluntary retirement savings and occupational compulsory retirement savings. Voluntary supplementary retirement savings are close to the “individual pension savings schemes” (UK) or the 401(k) pension plan (US). Occupational compulsory retirement savings refer to pension schemes offered by large firms, or pension schemes designed for self-employed.

2.2. Classification of private pension insurance in the Patrimoine Survey

The Patrimoine 2004 Survey distinguishes three types of life insurance products:

Pure life insurance: term, or whole-life, policy providing payments to beneficiaries if death occurs during the contract, nothing being paid in case of survival of the insured. The survey only takes into account policies taken out by individuals (group insurance contracts backing mortgage loans, or contracts subscribed within firms to cover death or disability at work are excluded). 52% of households and 27% of surveyed individuals are holding this type of contract.

Pure endowment insurance, annuities and endowment insurance (i.e. mix of term life insurance and term annuity): 17% of households and 30% of surveyed people are concerned.

Popular savings schemes (in French Plans d’Epargne Populaire - PEP), which are tax exempted savings schemes provided that the amount invested is kept during at least 5 years); banks and insurance companies can supply these PEPs; when a pure endowment insurance contract is nested in a PEP, the PEP is considered as an insurance vehicle. 10% of households surveyed and 5% of individuals are holding a PEP.

In this research, we take into account the endowment insurance and individual retirement savings since we were interested in the “saving” behaviour of the elderly (pure life insurance having no savings component). We have thus aggregated pure endowment insurance, annuities, and PEP on the one hand, and labelled such an aggregate “endowment insurance”. We have excluded occupational compulsory retirement savings. By definition, individuals cannot freely choose to hold occupational retirement schemes. Hence, such products are seldom offered by firms in France (only very few large firms do so), the French second pillar pension scheme being managed on a pay-as-go-basis. The holding rate of such products is thus very low (about 2%).

2.3. Methods to measure income inequality and poverty

We aim at measuring the poverty level and the inequalities among retired people, in order to analyse the impact of insurance endowment in preventing risk poverty. By using the Patrimoine survey, we select a sample of Retirees aged of 50 and more.

The Gini index is used to illustrate the inequality level among Retired People. It incorporates detailed shares data into a single measure, which summarizes the dispersion of income across the entire income distribution. The Gini index6 ranges from 0, indicating perfect equality (where everyone receives an equal share), to 1, perfect inequality (where all the income is received by only one recipient or group of recipients).

6 = −

∑

= ( − − )( + − ) N i i i i i x y y x Gini 1 1 1 1In order to take into account economies of scale- in consumption for instance- in the households, we use an adjusted income. It allows us to take into consideration the number of people living in the household. We assign the value of 1 for the first household member, 0.7 to each additional adult and of 0.5 to each child. This equivalence scale is known as the “Oxford equivalence scale”.

The poverty rate is calculated by considering 50% of the median income. The amount of the household income is not directly available in the Patrimoine survey, but incomes are crossed by ranges. Consequently we create the variable “income” equal to the median of the range and adjust this income to the size of the households using the Oxford equivalence scale. It allows us to calculate the adjusted income of individuals.

3. Private pension insurance and Poverty

Over the past years, France has experienced an increase in long term savings. As revealed by previous surveys such as Actifs financiers in 1992 and Patrimoine 1998, the Patrimoine 2003-2004 survey highlights a tendency for older households to have a higher saving rate leading to a sharp increase in the demand for life insurance endowment and retirement savings. In 1992, 39.5 % of households held private pension insurance contracts. In 1998, the holding rate reached 45.9 % and in 2004, 59%.

The growth of life insurance and retirement savings is particularly sensitive among elder households. Indeed, Patrimoine 2004 Survey shows that the life insurance and retirement savings holding increases with age until 70 and decreases afterwards (See table 1). However, this increase may be partially attributed to a wealth effect (See table 2).

Table 1 Insurance endowment per age in the Patrimoine Survey 50-59 years old 60-69 years old 70-79 years old 80 years old and more Total of the sample People without insurance endowment 97 755 807 367 2026 People holding insurance endowment 46 426 484 165 1121 N 143 1181 1291 532 3147

Table 2 Ranges of disposable income per age

Source: Author’s calculation using a sample of 3147 individuals, Patrimoine Survey. Less than 2500 euros 2500 to 5000 5000 to 7500 7500 to 9500 9500 to 12000 12000 to 14500 14500 to 20000 20000 to 25000 25000 to 30000 30000 to 36000 36000 to 48000 48000 to 72000 72000 and more Total of the sample 50-59 years old 1 2 1 5 4 8 26 17 25 20 21 12 1 143 60-69 years old 22 28 51 71 81 136 231 172 113 77 116 61 22 1181 70-79 years old 28 32 60 96 152 207 266 164 89 58 71 58 10 1291

80 years old and

more 14 18 50 61 66 62 94 60 33 18 32 18 6 532

In 2007, according to Eurostat, the poverty rate reaches 19% in the EU-25 and 13% in France for people of 65 and more.

We have seen for a person aged 65 years and leaving alone, the poverty rate represent 15.5% against 7.3% for household with the head aged 65 years old. In the context of pension reforms, we could anticipate a decreasing of the retirement income and, as a consequence, an increase of the poverty level among retirees.

By using the “Patrimoine Survey”, the poverty level and inequality are estimated. We aim at analyzing the relationship between the poverty and the holding of private pension insurance.

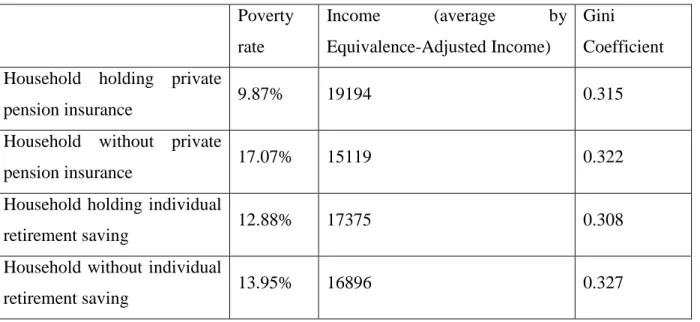

Our results show the poverty rate, in 2003, reach 7 500 euros. The poverty rate for the household holding private pension insurance is 9.87% against 17.07% for the household without private pension insurance. When we take into consideration the individual retirement saving, we obtain the same result: the poverty rate reach 12.88% for household holding these individual pensions against 13.95% for those without these products Cf. Table 2). Also the inequality seems to be less pronounced for household having the individual pension.

Table 3 Poverty/inequality when the head of household is retiree

Poverty rate Income (average by Equivalence-Adjusted Income) Gini Coefficient Household holding private

pension insurance 9.87% 19194 0.315

Household without private

pension insurance 17.07% 15119 0.322

Household holding individual

retirement saving 12.88% 17375 0.308

Household without individual

retirement saving 13.95% 16896 0.327

4.POVERTY, PENSION INSURANCE ANDSOCIO-DEMOGRAPHIC CHARACTERISTICS

In the second stage of the analysis we have tested the relationship between poverty, respondents’ pension insurance and socio-demographics characteristics.

Gender, marital status (married or single, widowed, divorced), the social and professional categories (blue collars, white collars, employees, self-employed) are considered. In order to capture the age effect, we have considered age groups, with a ten-year interval, from fifty to eighty old and over.

To analyse the longevity effect, the life expectancy at the age of fifty is considered. We also considered the area and the nationality (French and foreigner).

We take into account a dummy variable indicating whether households are indebted.

Indeed, property investments may provide a good vehicle for consumption at retirement. We have also considered a dummy variable indicating if the household are home ownership or not.

Home ownership may negatively affect the demand for endowment insurance and retirement savings if it is considered as a partial substitute for precautionary savings.

In order to observe if the existence of a pension life insurance might affect the poverty, insurance contract and popular saving schemes are taken into consideration.

In the first step, we have tested a Probit model explaining the probability to be poor. In the second step, we have constructed a bi-Probit model with the double regression: one with the probability to be poor and the other one, with the probability to hold private pension insurance in order to estimate de correlation between risk of poverty and life insurance holding among retirees.

The probit model may be formulated as:

(

poori)

Xibi uiob =1 = +

Pr (1)

i

u ~ N

( )

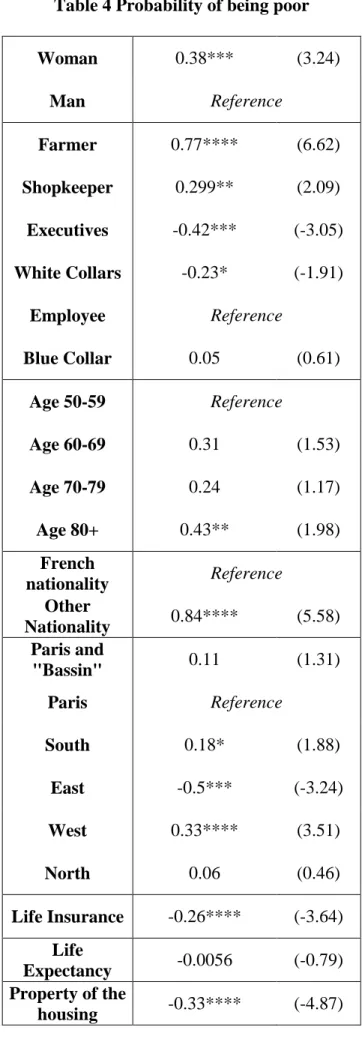

0,1The “age” variable refers to the age of the head of the household. The reference age group is 50-59, because it precedes the legal retirement age (which is 60 in France, to be entitled to full pay-as-you-go pension benefits). The results of the Probit estimation show the probability to be poor is large and significant at 80 years old.

As expected, for white collar and executives, there is a significant wealth effect. This variable could be considered as a proxy of income and education. The probability to be poor for white collar and executives is very weak contrary for blue collar, employees and farmer.

Also the marital status has a large effect: to be married or widowed avoid being poor contrary to single.

The effect of holding life insurance on the poverty level is statistically significant. The household having life insurance are above the poverty line. Being owner of his house also allows avoiding the risk of poverty. The coefficient of this variable is statistically significant and negative. It is also the case for the variable “debt”: indebted people tend to be less poor than people without personal debt. We could be surprised by this result, however, we could argue that indebted people were offered the possibility to contract a credit. On the opposite, the poorest people are more constrained.

On the contrary, we observe that people of foreign nationality tend to be poorer than French people. In the same time, the living location seems to be significant: living in the West or South part of the country tends to increase the risk of poverty compared to Paris, whereas people living in the East part know a less probability to be poor.

Table 4 Probability of being poor Woman 0.38*** (3.24) Man Reference Farmer 0.77**** (6.62) Shopkeeper 0.299** (2.09) Executives -0.42*** (-3.05) White Collars -0.23* (-1.91) Employee Reference Blue Collar 0.05 (0.61) Age 50-59 Reference Age 60-69 0.31 (1.53) Age 70-79 0.24 (1.17) Age 80+ 0.43** (1.98) French nationality Reference Other Nationality 0.84**** (5.58) Paris and "Bassin" 0.11 (1.31) Paris Reference South 0.18* (1.88) East -0.5*** (-3.24) West 0.33**** (3.51) North 0.06 (0.46) Life Insurance -0.26**** (-3.64) Life Expectancy -0.0056 (-0.79)

Personal Debt -0.32*** (-2.61) Children 0.14 (1.26) No Child Reference Married -0.45**** (-3.71) Divorced -0.3** (-2.17) Widowed -0.56**** (-4.7) Single Reference Cons -0.92*** -3.55 Obs: 3147 LR Chi2(23): 331.04 Pseudo_R2:0.144 Log Likelihood: -985.91 Legend: *p<0.1, **p<0.05, ***p<0.01, ****p<0.001

We now turn to the Bi-probit model considering the level of poverty simultaneously with the private pension insurance holding. We observe similar results concerning the estimation of the probability being poor. Our model may be expressed as:

(

poori)

Xibi ui ob =1 = + Pr (1)(

avi)

Xidi vi ob =1 = + Pr (2) → V N v u , 0 0The equations (1) and (2) are estimated simultaneously. The error terms follow a multivariate normal distribution, where V represents the residual covariance matrix, with ρ as the correlation coefficient of the residual u and v.

= 1 1

ρ

ρ

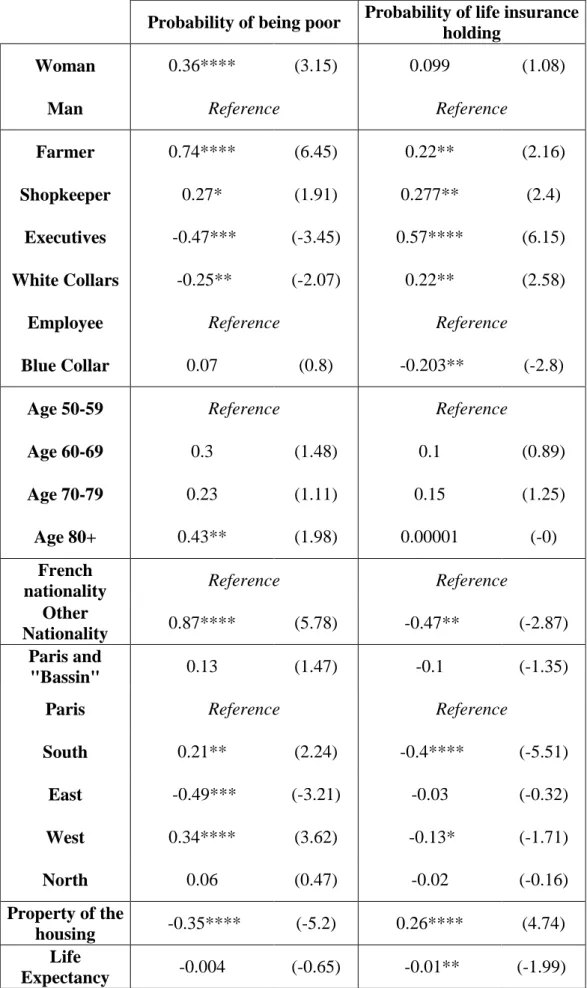

VConcerning the probability of life insurance holding, fewer variables seem to be significant. However, belonging to a specific social category impact the probability of having a life insurance. Blue collars tend to hold less life insurance than employees, whereas, the other categories hold more contract than them.

The probability to have a life insurance is significant and negative for foreign people, compared to French people.

Areas where people know a higher risk of poverty are also very significant in this regression. But people living in the south or in the east of France tend to have a less high probability to hold a life insurance, compared to the Parisians.

Being owner of his house also avoid the risk of poverty and increase the probability of life insurance holding.

Lastly, whereas the life expectancy seems to have not an impact on the poverty, it tends to have one on the probability to hold life insurance. This impact is statistically significant and negative. Having a high life expectancy tends to decrease the probability of having a life insurance. To calculate the life expectancy variable, we distinguished men and women. Statistically, we have observed that poverty risk is higher for women. Indeed, women living longer than men, the life expectancy result could be due to their lower life insurance holding.

Table 5: Biprobit: probability to be poor and to hold life insurance

Probability of being poor Probability of life insurance holding

Woman 0.36**** (3.15) 0.099 (1.08)

Man Reference Reference

Farmer 0.74**** (6.45) 0.22** (2.16)

Shopkeeper 0.27* (1.91) 0.277** (2.4)

Executives -0.47*** (-3.45) 0.57**** (6.15)

White Collars -0.25** (-2.07) 0.22** (2.58)

Employee Reference Reference

Blue Collar 0.07 (0.8) -0.203** (-2.8)

Age 50-59 Reference Reference

Age 60-69 0.3 (1.48) 0.1 (0.89)

Age 70-79 0.23 (1.11) 0.15 (1.25)

Age 80+ 0.43** (1.98) 0.00001 (-0)

French

nationality Reference Reference

Other

Nationality 0.87**** (5.78) -0.47** (-2.87) Paris and

"Bassin" 0.13 (1.47) -0.1 (-1.35)

Paris Reference Reference

South 0.21** (2.24) -0.4**** (-5.51) East -0.49*** (-3.21) -0.03 (-0.32) West 0.34**** (3.62) -0.13* (-1.71) North 0.06 (0.47) -0.02 (-0.16) Property of the housing -0.35**** (-5.2) 0.26**** (4.74) Life Expectancy -0.004 (-0.65) -0.01** (-1.99)

Personal Debt -0.31** (-2.52) -0.08 (-1.99)

Children 1.14 (1.26) -0.02 (-0.26)

No Child Reference Reference

Married -0.45**** (-3.68) -0.11 (-0.11)

Divorced -0.29** (-2.1) -0.1 (-0.82)

Widowed -0.55**** (-4.64) -0.05 (-0.51)

Single Reference Reference

Cons -1**** (-3.89) -0.45** (-2.52)

ρ -0.16**** (-3.79)

Likelihood-ratio test of rho=0: Chi2(1) = 14.46 P-value = 0.0001

Obs: 3147 LR Chi2(44): 459.2 Log Likelihood: -2930.34

Conclusion

The life insurance products have an important role to play in helping people manage their income into retirement.

The aim of this research was to analyze the effect of holding life insurance on the poverty. Our results indicate that the household having life insurance are above the poverty line.

The low level of public retirement pensions in France for some socio-occupational categories could be improved by helping saving (tax policy) these categories of households. Private insurance saving could be complementing efficiently the low level of State pension for women, blue-workers, foreigners and self-employed households. The social life-insurance programs could be developed in most countries where pension reforms are going to induce a low level of pension income.

For instance, in Germany, the introduction of the Reister-Rente in 2001 increased considerably the level of private savings for retirement. The Reister-Rente is a supplementary capital-based strongly State-supported private pension scheme. It was introduced in order to compensate for the reductions in the pension level of the statutory pension scheme. It takes into account the person’s revenue and the family size, and is available to the private and public sector equally. The Reister-Rente is considered to be part of the third pillar; however it could equally be considered part of the second pillar as individuals may ask for a Reister-Rente contract from their employers, the latter able to benefit from tax deductions.

References

Ando A. and F. Modigliani, (1963), The Life Cycle Hypothesis of Saving: Aggregate Implications and Tests, American Economic Review, 53 (March): 55-64.

Arrondel L., Masson A., Pestieau P., 2003, Epargne, Assurance Vie et Retraite, assurance, audit, actuariat edn.

Arrondel L. and A. Masson, (1996), Gestion du risque et comportements patrimoniaux, Economie et Statistique, n°296-297 : 63-89.

Attanasio O.P. and G. Weber, (1995), Is Consumption Growth Consistent With Intertemporel Optimisation? Evidence from the Consumer Expenditure Survey, Journal of Political Economy, 103(6): 1121-1157.

Auerbach A.J. and L.J. Kotlikoff, (1987), Life insurance of the Elderly: Its Adequacy and Determinants, in Work, Health, and Income among Elderly, Burtless G. (ed.), The Brookings Institution, Washington D.C.

Auerbach A.J. and Kotlikoff L.J., (1991), The Adequacy of Life Insurance Purchases, Journal of Financial Intermediation (June): 215-241.

Bernard P., N. El Mekkaoui de Freitas, A. Lavigne and R. Mahieu (2002) « Ageing and the Demand for Life Insurance: An Empirical Investigation using French Cross Section Data», Eurisco Working Papers, University Paris-Dauphine.

Bernheim D.B., L. Forni, J. Gokhale and L.J. Kotlikoff, (1999), The Adequacy of Life Insurance: Evidence from the Health and Retirement Survey, NBER WP n°7372.

Börsch-Supan, A. (2005), “Mind the Gap: The Effectiveness of Incentives of Boost Retirement Saving in Europe”, OCDE Economic Studies n° 39, OCDE, Paris.

Browning M. and A. Lusardi, (1996), Household Saving: Micro Theories and Micro Facts, Journal of Economic Literature, 34(4) : 1797-1855.

Caroll C.D., (1992), The Buffer-Stock Theory of Savings: Some Macroeconomic Evidence, Brooking Papers on Economic Activity, 2 : 61-156.

Cohen S., Lelièvre M., (2003), Niveau de vie et risque de pauvreté parmi les retraités des pays européens, Etudes et Résultats n°213, Drees.

Brown J.R., (2002), Redistribution and Insurance: Mandatory Annuitization with Mortality Heterogeneity, NBER Working Paper No. 9256.

Fédération Française des Sociétés d'Assurance (2004, 2009), Rapport annuel, Paris.

Hachon C., (2008), Do Redistributive Pension Systems Increase Inequalities and Welfare? February, WP.

Insee (1998), Enquête Patrimoine, Insee.

Insee (2003-2004) Enquête Patrimoine, Insee.

Whitehouse E., Zaidi A. (2008), Socio-economic Differences in Mortality: Implications for Pensions Policy, WP n°71, OECD.

Yaari (1965), «Uncertain Lifetime, Life Insurance and The Theory of the Consumer», Review of Economic Studies, n°32.