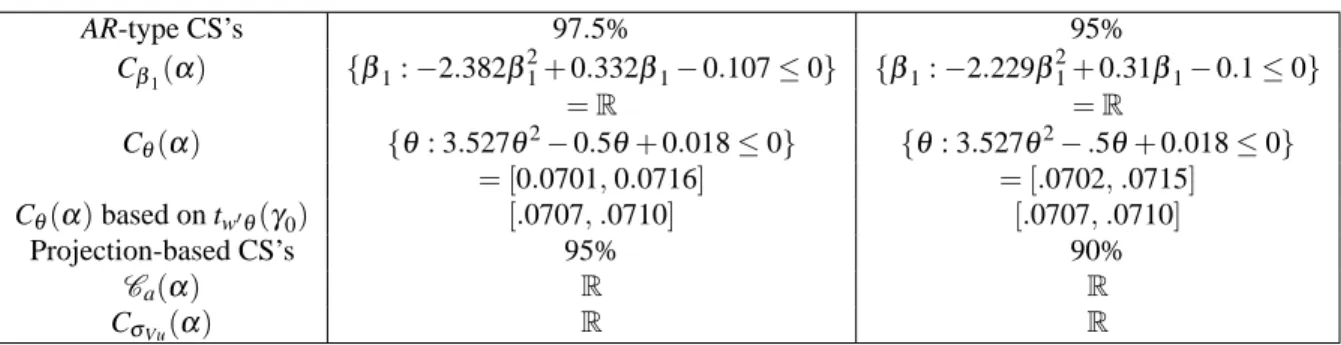

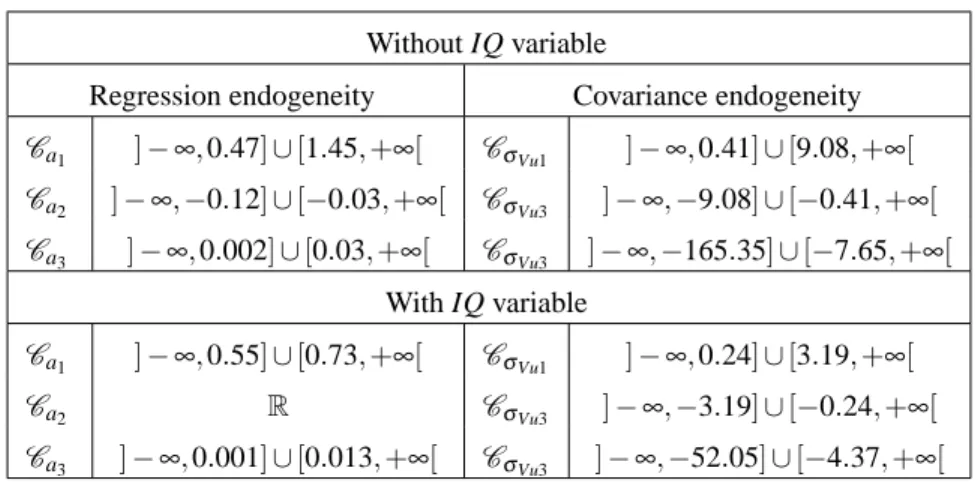

Identification-robust inference for endogeneity parameters in linear structural models

Texte intégral

Figure

Documents relatifs

The Hamiltonian Monte Carlo algorithm and a method based on a system of dynamical stochastic differential equations were considered and applied to a simplified pyrolysis model to

In the presence of small deviations from the model (Figure 2), the χ 2 approximation of the classical test is extremely inaccurate (even for n = 100), its saddlepoint version and

Robust and Accurate Inference for Generalized Linear Models:..

By starting from a natural class of robust estimators for generalized linear models based on the notion of quasi-likelihood, we define robust deviances that can be used for

Therefore, usual results for linear spectral method as the one given in Equation (4.8) cannot apply. Because the PLS filter factors can be larger than one, [FF93] proposed to bound

Estimating parameters and hidden variables in non-linear state-space models based on ODEs for biological networks inference... Estimating parameters and hidden variables in

Inspired by the Bayesian evidence framework proposed in [31] to solve noisy interpolation problems, we have derived a generic and reliable hierarchical model for robust

In addition to handling the relationship between observed data and the latent trait via the link and distribution functions, any system for expected and observed scale quantitative