1

THE ENGAGED ORGANIZATION:

HUMAN CAPITAL, SOCIAL CAPITAL, GREEN CAPITAL AND LABOR PRODUCTIVITY

Magali Delmas, University of California, Los Angeles1 and

Sanja Pekovic, University of Dauphine, Paris

DRAFT

ABSTRACT

In this paper, we develop a model of the engaged organization, which shows how human capital can interact with social and green capital to influence organizational outcomes, particularly labor productivity. We argue that engaged organizations, that facilitate knowledge sharing and learning, employee motivation and commitment to the organization, can demonstrate increased labor productivity. We test our hypotheses with French survey data that detail employee characteristics from 5, 210 respondents for 1,988 firms. Our results show that higher levels of labor productivity are associated with greater financial participation, interpersonal contact, inter-firm partnerships and proactive environmental management practices.

Keywords: labor productivity, social capital, green capital, human capital, intellectual capital

1 Contact: [email protected]

2

INTRODUCTION

The strategy literature has paid particular attention to how organizational resources and capabilities, including inter-firm relations and, to a lesser extent, environmental innovation, impact firm performance (Mowery, Oxley, & Silverman, 1996; Gulati, 1998; Dowell, Hart, & Yeung, 2000; Russo & Fouts, 1997). However, the strategy literature has only recently recognized the strategic importance of human resources (Koch & McGrath, 1996). In contrast, the human resources literature has devoted most of its attention to understanding how the development of human capital within the firm influences organizational outcomes such as labor productivity (Guthrie, 2001; Datta, Guthrie, & Wright, 2005). In this paper, we bridge these two literatures using a model of the engaged organization, which shows how human capital can interact with other forms of intellectual capital to influence organizational outcomes, particularly labor

productivity.

In the engaged organization, employees have high levels of interpersonal contact with other employees, and also have a stake in the firm’s financial returns. They are part of a broader organizational environment that goes beyond the boundaries of the firm to include alliances with other organizations and commitment to improving the natural environment. Our focus on the engaged organization unveils significant

interrelation among sources of human, social and green forms of capital. This is evident in the links revealed between the adoption of environmental and other organizational practices and corporate performance. In this way, we respond to the call made by some scholars to open the organizational black box in order to understand the organizational changes associated with “greening” a firm (Jackson, Renwick, Jabbour, & Muller-Camen, 2011; Delmas & Toffel, 2008).

We argue that engagement by employees and the firm with external organizations and the firm’s commitment to improving the natural environment through the adoption of proactive environmental practices lead to higher organizational performance. We discuss the ways in which engaged organizations can facilitate knowledge sharing and learning, employee motivation and commitment to the organization, and demonstrate increased labor productivity. We test our hypotheses with data obtained from French surveys that detail employee characteristics from 5, 210 respondents for 1,988 firms. Our results show that

3

higher levels of labor productivity are specifically associated with greater financial participation, interpersonal contact, inter-firm partnerships and proactive environmental management practices. Our study seeks to advance intellectual inquiry at the intersection of strategic management and the management of human capital. By describing how interactions among sources of human, social and green forms of capital can influence firm-level outcomes we hope to provide a deeper theoretical and empirical understanding of human-based organizational performance.

LITERATURE REVIEW

Human capital, a form of intellectual capital, is defined as “a unit level resource that is created from the emergence of individual’s knowledge, skills, abilities and other characteristics” (Ployhart & Moliterno, 2011: 128). Previous studies have argued that human capital manifests across organizational levels (Ployhart & Moliterno, 2011) and has a positive influence on competitive advantage (Edvinsson & Malone, 1997; Johnson, 1999; Stewart, 1997). Human capital can be at the core of a resource-based advantage if it is valuable, rare, and can be kept from rivals (Coff, 2002).

However, organizational behavior and organizational performance cannot be explained simply in terms of personal attributes. The individual’s behavior and performance will be determined by the organizational climate, the structure of the organization and the organization’s socialization processes as well as by individual characteristics (Tomer, 1990). The concept of social capital has been increasingly used to represent the “goodwill that is engendered by the fabric of social relations and that can be mobilized to facilitate action” (Adler & Kwon, 2002: 17). Social capital is correlated with human capital but social ties are distinct from education or training which have been used to measure human capital (Nahapiet & Ghoshal, 1998; Blyer & Coff, 2003). Social capital contributes to the organizational context for human capital and has proven to be a powerful factor explaining organizational performance such as innovation and inter-firm learning (Gabbay & Zuckerman, 1998; Kraatz, 1998). However, according to Payne, Moore, Griffis, and Autry (2011: 1): “While social capital has been applied at the individual, group and organizational levels of analysis, researchers have yet to embrace social capital as a multilevel lens to better understand management and organizational phenomena.”

4

More recently, the concept of green capital has been offered by Chen (2008) who defines it as the “employees’ stocks of knowledge, skills, capabilities, experiences, attitude, wisdom, creativities, and commitments about environmental protection or green innovation” (Chen, 2008: 275). An extensive literature has focused on explaining the determinants of organizational engagement beyond the firm to improve the natural environment through the adoption of environmental practices and standards (Delmas & Toffel, 2008). Understanding the relationship between the adoption of environmental practices and financial performance has been the focus of considerable research since the 1970s (Orlitsky, Schmidt, & Rynes, 2003; McWilliams & Siegel, 2011). However, the literature so far has focused mainly on the impact of the adoption of environmental practices at the macro level, and it has remained unclear exactly how these practices impact organizational effectiveness, employee productivity and green capital per se. Until now, mostly anecdotal evidence has been presented to support the argument that greater employee loyalty and productivity occur at environmentally or socially-responsible firms (Delmas & Pekovic, 2012). Recent research, though, shows that intellectual capital related to green innovation or environmental management has a positive impact on competitive innovation (Chen, 2008; Delmas, Hoffmann, & Kuss, 2011).

While research has defined these different forms of capital, and explored their influence on organizational performance, no study to date has combined them. Little research exists, for example, on the value of the organizational context in the development of human capital. Abell, Felin, and Foss are among those who suggest that: “substantial attention be paid to explanatory mechanisms that are located at the level of individual action and (strategic) interaction” (Abell, Felin, & Foss, 2008: 489). Similarly, while circumstantial evidence provided by consultants and managers describes the value of green capital in enhancing human capital engagement, rigorous research is scarce on this issue. In this paper we analyze the direct impact of sources of human, social and green types of capital on labor productivity and their interaction.

Scholars have used different measures of organizational performance. These include: human resource outcomes (turnover, absenteeism, job satisfaction), organizational outcomes (productivity, quality, service), financial accounting outcomes (ROA, profitability), and capital market outcomes, (stock price,

5

growth, returns) (Dyer & Reeves, 1995). According to Dyer and Reeves (1995), human resource strategies are most likely to directly impact human resource outcomes, followed by organizational, financial, and capital market outcomes. In this paper, we focus on organizational outcomes, looking more specifically at labor productivity as a reliable and widely used measure of the effect of human resources on organizational performance.

Samuelson and Nordhaus define labor productivity as “total output divided by labor inputs” (1989: 980). High labor productivity is therefore a desirable outcome. Labor productivity measures the extent to which the human capital is delivering value to the firm. A firm that excels in the creation of human capital resources should have people who are highly productive relative to the competition (Koch & McGrath, 1996; Porter, 1985).

The literature has emphasized the role of human skills and human capital on labor productivity. Human capital stock, accumulated through training activities, is one of the main factors of production (e.g., Lynch, 1994). Investment in human resources has been recognized as a significant source of competitive

advantage since such investments can lead to more effective employees (Porter, 1985). One of the key tools for investing in human resources is training (Jennings, Cyr, & Moore, 1995). Scholars have argued that training is profitable as it increases the specificity of human capital assets, making it more difficult for competitors to imitate (Koch & McGrath, 1996). Empirical evidence corroborates this conclusion and shows that training is positively associated with labor productivity improvement (Dearden, Reed, & Van Reenen, 2006; Conti, 2005; Zwick, 2004; Rennison & Turcotte, 2004; Koch & McGrath, 1996). In this paper, we propose a broader view of human capital management beyond the human resources department where firms not only provide employees with training to improve their knowledge and skills, but also encourage employees to engage in interpersonal contact with their colleagues and to have a stake in the success of the organization. We argue that employees engaged in these ways will be more

productive in organizations that are open to relations with other firms and that invest in environmental practices.

6 HYPOTHESES

Studying the engaged organization encompasses a wide perspective on human capital that derives from two main characteristics of the organization: First, it favors interconnections between employees and with other organizations. These connections support learning and the development of social capital. Second, the organization encourages employees to identify with its goals to increase employee commitment to the organization. This is achieved by providing employees with a financial stake in the organization and helping employees self-identify with the organization through the adoption of sustainable practices. In this way, the engaged organization addresses both the cognitive content of human capital (knowledge and experience) and the non-cognitive content of human capital (values and interests) as defined by Ployhart and Moliterno (2011).

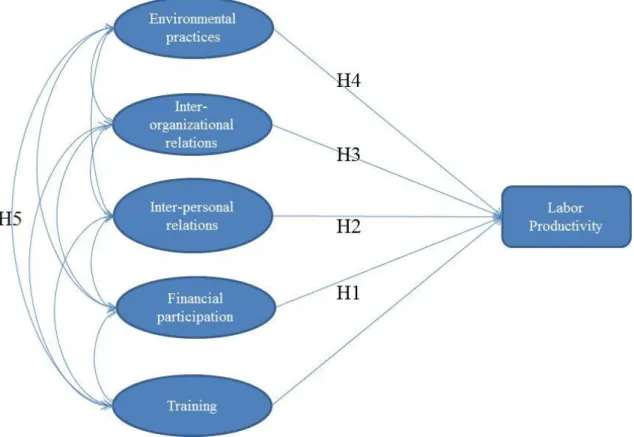

We capture these characteristics in a framework that includes human capital, social capital and green capital (see Figure 1 below). The framework combines individual level employee characteristics with organizational level characteristics. Our approach includes internal organizational characteristics of firms as well as firm relations with the competitive and natural environments. We describe the elements that favor employee engagement within the firm and its productivity, and we outline how firm engagement beyond its boundaries supports labor productivity. We also describe interactions between internal and external engagement. Our hypotheses are developed below.

***

Insert Figure 1 about here ***

Human capital engagement through financial participation

Profit sharing schemes provide employees with additional income based on the profitability of the firm (Florkowski, 1987). Scholars have argued that employee financial participation strengthens workers' commitment to the firm, reduces the need for costly monitoring, and increases work effort (Doucouliagos, 1995; Fitzroy & Kraft, 1987; Cable & Wilson, 1989, 1990; Wadhwani & Wall, 1990; Kruse, 1992). It is argued that employees, when they share in ownership, can think and act like owners (Pfeffer, 1998),

7

becoming more responsible and accountable for organizational outcomes. The “intrinsic” perspective suggests that employee ownership increases employee commitment to, and satisfaction with, the company and that the benefits of ownership are derived directly from the fact of ownership rather than from factors in the ownership scheme itself or in the organizational context. Other more instrumental perspectives argue that financial participation allows the employee to be a more significant participant in the organization and to influence decision-making leading to organizational effectiveness (Coyle-Shapiro, Morrow, Richardson, & Dunn, 2002). Here we argue that financial participation will facilitate the alignment of employee values and interests with those of the firm, and should amplify the content of human capital such as the

knowledge acquired through training, thus resulting in increased labor productivity. We therefore hypothesize the following:

Hypothesis 1: Employee financial participation is associated with greater labor productivity.

Employee and organization interactions and social capital

Interpersonal relations

In his seminal work, Kotter described how effective managers spend more than 80% of their time interacting with others, gathering and sharing information (Kotter, 1982). Beyond general management, others have since investigated the importance of interpersonal contacts on employee productivity (Luthans, 1988; Greve, Benassi, & Arne Dag, 2010). There are two main reasons to explain why increased

interpersonal contacts in an organization can lead to improved labor productivity. First, interpersonal contacts increase employees’ “social capital” defined as the ability to reach others, inside and outside the organization for advice and problem-solving (Greve et al., 2010). Such social capital helps employees engage in knowledge transfer and leads to innovative ideas that improve productivity (Mohrman & Novelli, 1985; Hamilton, Nickerson & Hideo, 2003; Greve et al., 2010). It also binds employee together to amplify knowledge, skills and abilities and results in enhanced productivity (Ployhart & Moliterno, 2011). Second, interpersonal contacts can promote employee job satisfaction and motivation, which in turn lead to increased productivity. Like any other social activity, work entails social needs and responses, such as the need for connection, cooperation, support and trust (Cohen & Prusak, 2001). Organizations that facilitate interpersonal contact among their employees provide an enhanced working environment that might lead

8

employees to give more to the firm and increase their productivity, resulting in overall improved organizational productivity (Banker, Field, Schroeder, & Sinha, 1996; Batt, 2004; Huselid, 1995). We therefore hypothesize the following:

Hypothesis 2: Increased interpersonal relations are associated with increased labor productivity. Inter-organizational relations.

Inter-organizational relations present shared meaning, commitment and norms of reciprocity that enable understanding and knowledge transfer among various actors (Gulati, 1995; Youndt, Subramaniam, & Snell, 2004). One of the main reasons that firms participate in inter-organizational relations or partnerships is to access know-how, important information and capabilities belonging to their alliance partners (Kale, Singh, & Perlmutter, 2000; Hamel, 1991; Khanna, Gulati, & Nohria, 1998). The interaction between the individual members of the partner organizations is an effective mechanism to transfer or learn “sticky” and tacit know-how across the organizations (von Hippel, 1988; Marsden, 1990). Inter-organizational relations can enhance social capital and provide access to rich and diverse sets of information (Koka & Prescott, 2002). Social capital coming from inter-organizational relations—in a similar fashion to social capital stemming from intra-firm interpersonal relations—helps employees engage in knowledge transfer and leads to innovative ideas that improve productivity. We therefore hypothesize the following:

Hypothesis 3: Inter-organizational relations are associated with greater labor productivity. Green capital and positive social identity

We define proactive environmental practices and strategies as those that seek to reduce the environmental impacts of operations beyond regulatory requirements (Sharma, 2000). One mechanism that can link the adoption of proactive environmental practices to labor productivity is the positive social identity that can be derived from working in a “greener” firm. As Ambec and Lanoie noted: “People who feel proud of the company for which they work not only perform better on the job, but also become ambassadors for the company with their friends and relatives, enhancing goodwill and leading to a virtuous circle of good reputation” (Ambec & Lanoie, 2008: 57).

9

The social identity theory suggests that an employee's self-concept is influenced by membership in an organization (Ashforth & Mael, 1989; Dutton & Dukerich, 1991). According to this theory, the employee would experience a positive self-identity when working in firms with a positive environmental reputation (Turban & Greening, 1997). Several studies have shown that involvement in social and environmental causes enhances an organization’s reputation (e.g., Hess, Rogovsky, & Dunfee, 2002; Delmas, 2002; Delmas & Montiel, 2009). It seems likely, then, that the adoption of proactive environmental practices by an organization would lead to a positive organizational reputation and have a positive impact on

employees’ work attitudes.

A positive corporate social identity may create a stronger emotional association between employees and their firm, resulting in enhanced labor productivity (Koh & Boo, 2001; Viswesvaran, Deshpande, & Joseph, 1998; Hess et al., 2002) and increased employee organizational commitment (Dutton, Dukerich, & Harquail, 1994; Jones & Hamilton Volpe, 2011; Brammer, Millington, & Rayton, 2010; Peterson, 2004). When employees have a strong positive social identification with their organization, their goals and those of the organization become increasingly integrated (Hall, Schneider, & Nygren, 1970), and we can expect significant overall improvement in labor productivity as a result. We therefore hypothesize that the adoption of proactive environmental practices will enhance labor productivity.

Hypothesis 4: The adoption of environmental practices is associated with greater labor productivity.

The engaged organization

While we have argued that human capital, social capital and green capital have a direct impact on labor productivity, we need to consider that these different forms of intellectual capital do not function independently but synergistically and enhance each other.

Financial participation has been described as a way to enhance cooperation among employees. The idea is that employee participation in the profits of the firm will induce workers to internalize the positive

externalities gained from the individual decision and to cooperate in interdependent tasks (Fitzroy & Kraft, 1986, 1987). In other words, financial participation might motivate employee engagement with other employees and lead to enhanced inter-organizational relations and social capital.

10

Scholars have argued that social ties at one level of the organization influence a lower or higher level of the organization (Moliterno & Mahony, 2010). For example, internal social capital has been shown to

strengthen external social capital through, for example, enhanced supplier relations (Asanuma, 1985; Baker, 1990; Dore, 1983; Gerlach, 1992; Helper, 1990; Smitka, 1991; Uzzi, 1997), and inter-firm learning (Kraatz, 1998).

The adoption of proactive environmental practices, which enhance green capital, has been shown to relate to other organizational capabilities involving social capital, such as knowledge acquisition, assimilation, and transformation (Delmas et al., 2011) or the adoption of stronger inter-firm relations such as supply chain partnerships (Delmas & Montiel, 2009). The adoption of environmental practices could also affect training and inter-firm relations (Khanna & Anton, 2002). For example, one of the basic requirements to adopt the ISO 14000 international management system standard is to provide job-appropriate employee training, and several authors have shown that ISO certification is an important determinant of training efforts within the organization (Blunch & Castro, 2007; Ramus & Steger, 2000). We therefore hypothesize that sources of human, social and green forms of capital interact with each other.

Hypothesis 5: Sources of human, social and green capital interact positively to affect labor productivity.

The hypothesized relations are described in Figure 2. In addition to the effect of training on labor

productivity, we identify the effect of financial participation, inter-personal relations, inter-organizational relations and environmental practices on labor productivity as well as the interaction between these sources of human, social and green capital.

***

Insert Figure 2 about here ***

11 METHOD Data

To test our hypotheses, we used data from the French Organizational Changes and Computerization’s (COI) 2006 survey.2 The COI survey is a matched employer-employee dataset on organizational change and computerization from the National Institute for Statistics and Economic Studies (INSEE) and the Ministry of Labor, and the Center for Labor Studies (CEE). The survey benefited from a high response rate of 86% and contains 7,700 firms that are representative of the population of French firms from all

industries except agriculture, forestry and fishing. Each firm fills in a self-administered questionnaire about information technologies and work organizational practices in 2006, and changes that have occurred in those areas since 2003, as well as the goals driving decisions to implement organizational changes and the economic context in which those decisions were made. Within each surveyed firm, employees were randomly selected and asked about their personal socio-economic characteristics, as well as information about their job and position within the organization. The original dataset includes 14,369 employees. In order to obtain information on employee value-added activities, production sold and employee profit sharing, the COI survey results were merged with two other databases: the 2006 Annual Enterprise Survey (EAE) and the Elaboration of Enterprise Annual Statistics from 2008 (ESANE). The Annual Enterprise Survey is a mandatory survey conducted by the French Ministry of Industry to collect data on firm characteristics such as business activities, size and location. We used a sample comprising 80,000 enterprises.

Additionally, the Annual Statement of Social Data (Déclarations Annuelles de Données Sociales, DADS) is used to obtain information about wages and working hours. It contains administrative documents filled in by employers and reported to the Social Security and Tax Agencies. Some DADS information has been collected every year since 1950; the current system was first used for declarations relating to 1993. The DADS processing system provides researchers with a type of ongoing census of employee wages, number

2

More details about the design and scope of this survey are available on www.enquetecoi.net: Survey COI-TIC 2006-INSEE-CEE/Treatments CEE.

12

of days worked during the course of each year, qualifications, occupation, duration of employment, etc. The results are usually available 15 months after the end of the reporting year.

In order to obtain information about the adoption of environmental proactive practices, we merged the COI data with The Community Innovation Survey (CIS). The CIS survey was administered by the French Institute for Statistics and Economic Studies over the period 2006-2008; the survey is based on the OECD Oslo Manual. Firms answered questions regarding innovations they had introduced within the previous three years. The questionnaire was sent to 25,000 firms and brought another very high response rate at 81%. The CIS survey is mandatory for firms with more with 250 or more employees, bringing more important representation of firms with more than 250 employees. As a result of the data merges, our sample includes 5, 210 observations for 1, 988 firms. The average number of respondents per firm is 3, ranging from 1 to 12. We compared our sample with the representative sample from COI based on wages, size and sector covered. The only difference stems from size of the firms in our sample, which are

significantly larger (p<0.05). Measures

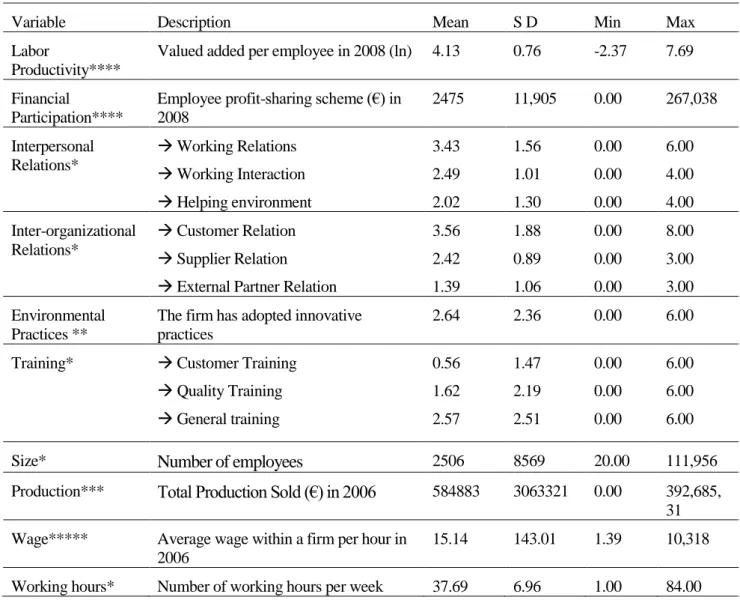

Labor Productivity. Drawing on prior research (e.g., Salis & Williams, 2010), we measure labor

productivity as the firm’s value added divided by the number of employees. Value added was measured in 2008 and is recorded in the ESANE database; the number of employees was obtained from the COI database.

Note that the dependent variable was measured in 2008 and the independent variables in 2006 to help control for reverse causality.

Financial Participation. The financial participation is a share of firm profit paid to employees. We introduced a variable representing employee financial participation in Euros.

Interpersonal Relations. To assess the level of interpersonal relations inside the firm we use three categories. The first category, working relations, is based on the following information: employee works regularly with (1) supervisor; (2) subordinates; (3) colleagues from the same firm; (4) different

13

following: employee has occasion to discuss different issues with colleagues inside the firm (3) frequently (2) occasionally (1) never or almost never; employee is part of a working group such as a project, problem-solving, pilot or brainstorming group; employee attends meetings. The helping environment category is based on the following items: employee participates in work task distribution (3) often (2) sometimes (1) never or almost never; and employee helps colleagues with work tasks (3) often (2) sometimes (1) never or almost never. We conducted an exploratory principal components factor analysis on these three

interpersonal relations measures. The three variables load on one factor explaining 70% of the variance. Inter-organizational Relations. To measure inter-organizational relations, we created three indicators: customer relation, supplier relation and external partner relations. The customer relation indicator consists of the following 8 items: (1) the firm uses labeling goods and services; (2) the firm is engaged in delivering or supplying goods or services according to a fixed deadline; (3) the firm is engaged in responding to claims or supplying after-sales service according to a fixed deadline; (4) the firm operates a contact or call center for clients; (5) the firm uses integrated IT management of customer relations; (6) the firm uses goods or services catalogues and price lists on a website; (7) the firm uses online sales; (8) the firm uses tools for sales via an electronic marketplace. The supplier relation indicator includes the following three items: (1) the firm selects suppliers via formal tender; (2) the firm has a long term relationship with certain suppliers; (3) the firm contracts with certain suppliers to deliver goods or services according to a fixed deadline. The external partner relation consists of the following three items: the firm has established R&D collaborations with (1) private businesses or laboratories; or (2) the Center for National Scientific

Research, universities or other public organizations; (3) the firm studies client expectations, behavior or satisfaction. We ran an exploratory principal components factor analysis on the three inter-organizational relations measures. The three variables load on one factor, which explains 68% of the variance.

Environmental practices. In order to measure a firm adoption of proactive environmental practices, we constructed a variable which consists of the following: the firm has adopted innovative practices to (1) reduce resource and/or material per unit of production (2) reduce energy use; (3) reduce firm’s CO2 ‘footprint’ (total CO2 production); (4) replace materials with less polluting or hazardous substitutes; (5) reduce soil, water, noise, or air pollution; (6) recycle waste, water, or materials.

14 We also included several control variables.

Training. Training has often been used as a proxy for human capital (e.g., Hatch & Dyer, 2004; Skaggs & Youndt, 2004). Therefore, we constructed three specific training indicators: customer oriented training, quality oriented training and general oriented training. Each training indicator includes the following components: (1) customer/quality/general training received; (2) year of training received. We ran an exploratory principal components factor analysis on the four measures. The three variables load on one factor, which explains 76.9% of the variance.

Size. The literature finds that firm size is a significant determinant of labor productivity (e.g., Zwick, 2004; Pfeffer & Langton, 1993). Therefore, we include firm size as measured by the number of employees within the firm.

Production. The financial strength of the firm leads to productivity improvement (Dearden et al., 2006). We therefore introduce a variable representing the total value of production sold in Euros.

Wage. Wages are found to have a significant effect on labor productivity (e.g., Alexander, 1993). We therefore include a variable representing the average wage paid by firms.

Working Hours. Following previous research (e.g., Sousa-Poza & Ziegler, 2003), we include a variable that indicates employee working hours.

The variables used in estimation, their definitions and sample statistics are presented in Table 1. ***

Insert Table 1 about here ***

Structural model. We employed structural equation modeling (SEM, AMOS Version 21, via maximum likelihood estimates) because of the ability of this technique to analyze models based on several latent variables and to model and test complex patterns of relationships (Hardy & Bryman, 2004). Structural modeling addresses structural and measurement issues frequently found in survey-designed research and is increasingly used in strategic-management research (Capron, 1999; Cordano & Frieze, 2000; Delmas & Toffel, 2008; Delmas et al., 2011; Sharma, 2000; Shook, Ketchen, Hult, & Kacmar, 2004; Simonin, 1999). The construction of each latent variable can be depicted by a set of linear equations of the form:

15 i p ip i i

x

x

Y

0

1

1

...

Similarly, the relation between the different latent variables can be described with a set of linear equations of the same form. The equations system is solved under the side condition to minimize the overall variance error. Often, different letters are used to distinguish between the latent and observable variables. For simplicity, and because we focus on the relation between the latent variables only, we use a single notation. As such, in our case the equations system between our main variables can be described as:

LB FP IR IOR EI CON LB

LP

x

x

x

x

x

Where

LP

presents labor productivity,

LBreflects a potential systematic deviation from the neutral level,FP

reflects the effect of financial participation on labor productivity ,

IR reflects the effect ofinterpersonal contacts on labor productivity,

IOR reflects the effect of inter-organizational partnership onlabor productivity,

EP reflects the effect of environmental practices on labor productivity,

CON reflects the effect of control variables such as training, size, total production, wage and working hours on labor productivity and finally

LP depicts the error in the variance that cannot be explained by any of thevariables.

Structural diagnostics. Based on a number of tests, we found a good overall fit for the model. We calculated the root mean squared error of approximation (RMSEA), an estimate of the discrepancy between the original and reproduced covariance matrices in the population (Steiger, 1990). In our model, the RMSEA of 0.04 is within an acceptable range (Cudeck & Browne, 1983). Likewise, we found an incremental fit index (IFI) (Bollen, 1989) of 0.95, a Tucker Lewis index (TLI) (Tucker & Lewis, 1973) of 0.92, and a comparative fit index (CFI) (Bentler & Bonett, 1980) of 0.95. Each of these indices is above the common threshold of 0.90 that designates an acceptable fit. In sum, these structural diagnostics indicate a very good relative fit of the theoretical model to the underlying data.

RESULTS

The measurement model refers to the construction of latent variables from observable items. In our case, we constructed three latent variables from 10 items. First, we conducted exploratory factor analyses on the items for each of the potential latent variables that showed suitable loading of each of the items on the

16

three factors. Second, we tested the measurement model by examining individual item reliability, internal consistency, and discriminant validity (see Table 2). The measurement model provided acceptable item reliability, all of the item loadings being statistically significant (p<0.001).

***

Insert Table 2 about here ***

As Table 3 illustrates, the results provide significant support for the hypothesized relations. There is a significant positive path between the influence of financial participation and labor productivity ( = 0.25 p<0.001), providing support for hypothesis 1.3 When financial participation goes up by 1 standard deviation, productivity goes up by 0.25 standard deviations or 6 % of the average productivity. Likewise, the significant positive relationship between interpersonal relations and labor productivity ( = 0.18; p<0.001) provides support for Hypothesis 2. When the variable interpersonal relation goes up by 1

standard deviation, productivity goes up by 0.18 standard deviations or 4.5 % of the average productivity. Regarding hypothesis 3, the variable inter-organizational relations is also significant and positive in predicting labor productivity ( = 0.11 p<0.001). When the variable inter-organizational relations goes up by 1 standard deviation, productivity goes up by 0.11 standard deviations or about 2% of the average productivity. Finally, the variable environmental practices is significant and positive at predicting labor productivity ( = 0.08 p<0.001) and confirms hypothesis 4. When the environmental practices variable goes up by 1 standard deviation, productivity goes up by 0.08 standard deviations or about 2% of the average productivity.

***

Insert Table 3 about here ***

17

Hypothesis 5 predicted positive interactions between the independent variables. Our results show positive and significant correlations between financial participation, interpersonal relations, inter-organizational relations and environmental practices (p<0.001). However, there was a slightly lower relationship between financial participation and training (p>0.05).

Controls. The variable representing training is positive and significant (p>0.05). The variable size is negative and significant (size = -4.69 p<0.001) indicating that smaller firms tend to be more productive. The variable working hours is positive and significant indicating higher productivity with more working hours ( = 0.14 p<0.001). However, the variable wage is not significant (p>0.10).

Alternative models. To compare our model to a more classic test of the effect of high work systems on labor productivity, we developed an alternative model in which we included training and financial participation and omitted the other hypothesized relations (interpersonal relations, inter-organizational relations and environmental practices). In this model the significance of the direct relationship between training and labor productivity increases ( = 0.13 p<0.001). The significance of financial participation remains unchanged ( = 0.27 p <0.001). We also used the nested model comparison procedure to test whether the inclusion of our variables improve the model. The results indicate a significant difference between the two models and a decrease in the fit indices with the more conventional model (p<0.001). In sum, our original model adds significant explanatory power to a more conventional approach.

Industry effects. In order to account for potential industry differences (Datta et al., 2005), we ran the model for the service and manufacturing sectors separately. In our sample, we have 2,175 observations from the service sector. The results of the service sector analysis yield fit indices and coefficients similar to those of the main model. However, the variable training lost its significance (p>0.10) and the variable environmental practices reduced its significance (p<0.015) (Appendix A). We also found a reduced correlation between training and financial participation as well as between interpersonal contacts and environmental practices (p>0.10). In contrast, the model for the 3,041 manufacturing observations has a reduced significance for interpersonal relations (p>0.1) but an increased significance for the training

18

variable ( = 0.15 p<0.01) (Appendix B). All the other variables are similar to those of the model with the full sample.4

Robustness. To ensure the robustness of our analysis, we validated the findings using a number of alternative approaches. First, since our data provides information on multiple individuals within each organization, there is the potential for correlation of errors across individuals within each organization. We therefore trimmed our sample and used only a randomly chosen individual respondent per firm in our estimations. There is no significant difference in the results between the two samples except that the training variable is less significant (p<0.10). We also averaged the employee level responses and re-run the analysis. There was no difference in this analysis with the main analysis presented in this paper. 5 Second, a potential concern derives from heterogeneity within our sample that is not controlled for in our structural equation model. Specifically, because our sample includes facilities from several sub-industries, and structural equation modeling techniques do not allow for industry dummies, it is possible that unobserved differences between these industries may account for some of our results. To test whether our results were sensitive to unobserved industry differences, we estimated regression equations corresponding to the paths of the structural equations. The results of these regression analyses confirmed the findings of the structural model. All hypothesized relations remain statistically significant (p<0.001) with the predicted sign.6 In summary, we find that financial participation, interpersonal relations, inter-organizational relations and environmental practices have a positive and significant impact on labor productivity. In addition we find a significant correlation between these variables with the exception of financial participation.

DISCUSSION

Our findings show that labor productivity is increased in an open organizational context where human capital interacts with social and green forms of capital. We argue that such interaction facilitates the development of both employee knowledge and experience as well as favors the alignment of employee values and interests. Our results show that our full model that integrates the sources of human capital,

4 Analyses at a more refined sectoral level yield unsatisfactory fit indices due to the lower number of observations and are not reported

5

Results available from the authors.

19

social and green capital yield superior significance as compared to a more limited model of human capital management.

Analysis of the engaged organization is enriched but also complicated by the need to consider multiple levels of analysis. Inter-organizational relations and the adoption of environmental practices occur at the firm level. However, as our model confirms, an understanding of the way such practices lead to firm level performance must incorporate constructs at the level of the individual and relations among individuals. These findings support the idea that there is a need to modify the scope and nature of human capital management processes to include a broader firm perspective. Our study contributes to both the human resource and strategy literature by bringing both individual and firm level perspectives together. Our findings have important managerial implications. They indicate interdependencies among multiple levels of strategy that firms can learn how to manage. Our analysis also points out a potential enhanced role for human resources in advancing sustainability. Currently, only a small percentage of human resource departments are responsible for creating sustainability strategy (SHRM, 2011). Sustainability is still within the purview of corporate strategy, health and safety, and/or the regulatory departments. However, a better integration of sustainability issues in the fabric of the organization can enhance employee engagement and productivity.

Critics of this approach might be concerned that employees in engaged organizations are more likely to find jobs somewhere else, leading to a higher voluntary turnover (Dess & Saw, 2001). However, as we argued, in engaged organizations, interpersonal and inter-organizational ties that could facilitate voluntary turnover, are combined with systems to encourage employee social identification and align employee’s interests with the goals of the organization. This combination should facilitate employee commitment to the organization and limit employee voluntary departure. This is consistent with Kale et al. (2000) who provide empirical evidence that social capital based on mutual trust and interaction at the individual level between alliance partners creates a basis for learning and know-how transfer across the exchange interface. This curbs opportunistic behavior by alliance partners, thus preventing the leakage of critical know-how. The benefits of the engaged organization are more likely to be felt by an organization reliant on knowledge management and operating in dynamic contexts. Indeed such environments are more likely to benefit from

20

flexible human resources who can adapt to changing requirements (Wright & Snell, 1998). Employees in engaged organizations, who benefit from ties with other organizations, should be more responsive than those who work in more recluse organizations. Organizations that operate in more stable environments may experience fewer benefits. Our results indicate, for instance, that interpersonal relations are less significant, and that training is more significant in manufacturing as compared to the whole sample. Interestingly, the adoption of proactive environmental practices remains a strong predictor of labor productivity in both the service and manufacturing contexts. This raises the question of which

configuration of human, social and green capital is the most effective and in what context. Further research could use such a configurational approach (Wright & McMahan, 1992).

We also contribute to the literature on social capital by empirically testing cross-level relations between individual level social capital and outcomes at the collective level. Although most theoretical models of social capital incorporate cross-level relations between individual level social capital and outcomes at the collective level, very few articles have examined cross-level relations empirically (Moliterno & Mahony, 2010; Payne et al., 2011). To represent social capital, we adopted Adler and Kwon’s (2002) notion of internal and external ties and more specifically individual/internal (interpersonal relations within the firm) and collective/external (inter-organizational relations). Further research could look at other types of social capital such as collective/internal and individual/external. We also measured sources of social capital rather than actual social capital.

Our results show that our training variable, used conventionally to assess human capital, loses some significance in some of our analyses. It is possible that other factors might be more relevant to measure as a source of human capital. Further research should identify if other human resource practices, such as rewards or performance appraisal, have a more significant effect than training when included in our model. Our research is not without limitations. First, our analysis was limited to the French context, and we were limited in identifying specific external market and regulatory conditions. Since scholars have identified international institutional differences regarding the implementation of environmental practices, future research could explore similar questions using a contingency approach in an international setting (Aragon-Correa, & Sharma, 2003; Delmas & Montes-Sancho, 2011). Second, our analysis studies the existence of

21

interdependence of different forms of intellectual capital rather than causality links between these. Further research could undertake a dynamic analysis to understand the steps of the development of the engaged organization. It is possible, for example that some organizations start with environmental innovation while others begin opening their organization through inter-organizational relations. Further research could also investigate how the characteristics of the engaged organization influence other organizational performance variables such as voluntary turnover, innovation or profit.

REFERENCES

Abell, P., Felin, T., & Foss, N. 2008. Building microfoundations for the routines, capabilities, and performance links. Managerial and Decision Economics, 29: 489–502.

Adler, P., & Kwon, S. 2002. Social Capital: Prospects for a New Concept. Academy of Management Review, 27(1): 17-40.

Alexander, C. 1993. The changing relationship between productivity, wages and unemployment in the UK. Oxford Bulletin of Economics and Statistics, 55(1): 87-102.

Ambec, S., & Lanoie, P. 2008. When and Why Does It Pay To Be Green. Academy of Management Perspective, 23: 45-62.

Aragon-Correa, J. A., & Sharma, S. 2003. A contingent re source-based view of proactive corporate environmental strategy. Academy of Management Review, 28: 71– 88.

Asanuma, B. 1985. The organization of parts purchases in the Japanese automotive industry. Japanese. Economic Studies, 13: 32 -78.

Ashforth, B.E., & Mael, F. 1989. Social identity theory and organization. Academy of Management Review, 14: 20–39.

Baker, W. 1990. Market networks and corporate behavior. American Journal of Sociology, 96: 589-625. Banker, R.E., Field, J.M., Schroeder, R.G., & Sinha, K. K. 1996. Impact of Work Teams on

Manufacturing Performance: A Longitudinal Field Study. Academy of Management Journal, 39(4): 867–890.

Batt, R. 2004. Who benefits from teams? Comparing workers, supervisors and managers. Industrial Relations, 43(1): 183–212.

Bentler, P.M., & Bonett, D.G. 1980. Significance Tests and Goodness of Fit in the Analysis of Covariance-Structures. Psychological Bulletin, 88: 588-606.

Blunch, N.-H., & Castro, P. 2007. Enterprise-level training in developing countries: do international standards matter? International Journal of Training and Development, 11(4): 314-324.

Blyer, M., & Coff, R. 2003. Dynamic capabilities, social capital, and rend appropriation: ties that split ties. Strategic Management Journal, 24: 677-686.

Brammer, S., Millington, A., & Rayton, B. 2010. The contribution of corporate social responsibility to organizational commitment. The International Journal of Human Resource Management, 18(10): 701-1719.

Cable, J., & Wilson, N. 1989. Profit sharing and productivity: An analysis of UK engineering companies. Economic Journal, 99: 366–375.

Cable, J., & Wilson, N. 1990. Profit sharing and productivity: some further evidence. Economic Journal, 100: 550–555.

22

Capron, L. 1999. The long-term performance of horizontal acquisitions. Strategic Management Journal, 20: 987-1018.

Chen, Y.S. 2008. The positive effect of green intellectual capital on competitive advantages of firms. Journal of Business Ethics, 77: 271-286.

Coff, R. W. 2002. Human capital, shared expertise, and the likelihood of impasse in corporate acquisitions. Journal of Management, 28(1): 107–128.

Cohen, D., & Prusak, L. 2001. In Good Company. How social capital makes organisations Work. Boston: Harvard Business School Press.

Conti, G. 2005. Training, productivity and wages in Italy. Labor Economics, 12: 557-576. Cordano, M., & Frieze, I.H. 2000. Pollution reduction preferences of US environmental managers:

Applying Ajzen's theory of planned behavior. Academy of Management Journal, 43: 627-641. Coyle-Shapiro, J.A.-M., Morrow, P.C., Richardson, R., & Dunn, S.R. 2002. Using Profit Sharing to

Enhance Employee Attitudes: A Longitudinal Examination of the Effects on Trust and Commitment. Human Resource Management, 41: 423–39.

Cudeck, R., & Browne, M.W. 1983. Cross-Validation of Covariance-Structures. Multivariate Behavioral Research, 18:147-168.

Datta, D.K., Guthrie, J.P., & Wright, P.M. 2005. Human resource management and labor productivity: does industry matter. Academy of Management Journal, 48(1): 135–145.

Dearden, L., Reed, H., & Van Reenen, J. 2006. The Impact of Training on Productivity and Wages: Evidence from British Panel Data. Oxford Bulletin of Economics and Statistics, 68: 397-421. Delmas, M., & Pekovic, S. 2012. Environmental Standards and Labor Productivity: Understanding the

mechanisms that sustain sustainability. Journal of Organizational Behavior, DOI: 10.1002/job.1827.

Delmas, M. 2002. The Diffusion of Environmental Management Standards in Europe and in the United States: an institutional perspective. Policy Sciences, 35(1): 91-119.

Delmas, M., & Montes-Sancho, M. 2011. An Institutional Perspective on the Diffusion of International Management System Standards: the Case of the Environmental Management Standard ISO 14001. Business Ethics Quarterly, 21(1): 103-132.

Delmas, M., Hoffmann, V. H., & Kuss, M. 2011. Under the Tip of the Iceberg: Absorptive capacity, environmental strategy and competitive advantage. Business & Society, 50: 116-154.

Delmas, M.A., & Toffel, M.W. 2008. Organizational responses to environmental demands: Opening the black box. Strategic Management Journal, 29:1027-1055.

Delmas, M., & Montiel, I. 2009. Greening the Supply Chain: When is Customer Pressure Effective? Journal of Economics and Management Strategy, 18(1): 171-201.

Dess, G.G., & Shaw, J.D. 2001. Voluntary turnover, social capital, and organizational performance. Academy of Management Review, 26: 446–456.

Dore, R. 1983. Goodwill and the spirit of market capitalism. British Journal of Sociology, 34: 459-482. Doucouliagos, C. 1995. Worker Participation and Productivity in Labor-Managed and Participatory

Capitalist Firms: A Meta-Analysis. Industrial and Labor Relations Review, 49(1): 58-78. Dowell, G., Hart, S., & Yeung, B. 2000. Do corporate global environmental standards create or destroy

market value? Management Science, 46: 1059-1074.

Dutton, J. E., & Dukerich J. M. 1991. Keeping an eye on the mirror: image and identity in organisational adaptation. Academy of Management Journal, 34: 517–554.

Dutton, J.E., Dukerich, J.M., & Harquail, C.V. 1994. Organizational images and member identification. Administrative Science Quarterly, 39: 239-263.

23

Dyer, L., & Reeves, T. 1995. HR strategies and form performance: what do we know and where do we need to go. International Journal of Human Resource Management, 6(3): 656-670.

Edvinsson, L., & Malone, M.S. 1997. Intellectual Capital. New York: Collins.

Fitzroy, F. R., & Kraft, K. 1987. Cooperation, productivity and profit sharing. Quarterly Journal of Economics, 102(1): 23-35.

Fitzroy, F. R., & Kraft, K. 1986. Profitability and Profit-Sharing. Journal of Industrial Economics, 35(2): 113-130.

Florkowski, G.W. 1987. The Organizational Impact of Profit Sharing. The Academy of Management Review, 12: 622-636.

Gabbay, S. M., & Zuckerman, E.W. 1998. Social Capital and opportunity in corporate R&D: The contingent effect of contact density on mobility expectations. Social Science Research, 27: 189-217.

Gerlach, M.L. 1992. Alliance capitalism: The social organization of Japanese business. Berkeley: University of California Press.

Greve, A., Benassi, M., & Arne Dag, S. 2010. Exploring the contributions of human and social capital to performance. International Review of Sociology, 20(1): 35-5.

Gulati, R. 1995. Social Structure and Alliance Formation Patterns: A Longitudinal Analysis. Administrative Science Quarterly, 40:619-652.

Gulati, R. 1998. Alliances and networks. Strategic Management Journal, 19: 293–317.

Hall, D.T., Schneider, B., & Nygren, H.T. 1970. Personal factors in organizational identification. Administrative Science Quarterly, 15: 176-190.

Hamel, G. 1991. Competition for competence and inter-partner learning within international strategic alliances. Strategic Management Journal, Summer Special Issue, 12: 83–103.

Hamilton, B. H., Nickerson, J. A., & Hideo, O. 2003. Team Incentives and Worker Heterogeneity: An Empirical Analysis of the Impact of Teams on Productivity and Participation. Journal of Political Economy, 111(3): 465-497.

Hardy, M.A., & Bryman, A. 2004. Handbook of data analysis. SAGE: London: Thousand Oaks, Calif. Hatch, N.W., & Dyer, J. H. 2004. Human capital and learning as a source of sustainable competitive

advantage. Strategic Management Journal, 25:1155-1178.

Helper, S. 1990. Comparative supplier relations in the U.S. and Japanese auto industries: An exit voice approach. Business Economic History, 19: 153-162.

Hess, D., Rogovsky, N., & Dunfee, T. 2002. The next wave of corporate community involvement: corporate social initiatives. California Management Review, 44(2): 110-125.

Huselid, M.A. 1995. The impact of human resource management practices on turnover, productivity, and corporate financial performance. Academy of Management Journal, 38: 635-672.

Jackson, S. E., Renwick, D. W. S., Jabbour, C. J. C., & Muller-Camen, M. 2011. State-of-the-art and future directions for green human resource management: Introduction to the special issue. Zeitschrift für Personalforschung, (German Journal of Research in Human Resource Management), 25 (2): 99-116.

Jennings, P.D., Cyr, D., & Moore, L. F. 1995. Human resource management on the Pacific Rim: An integration. In L. F. Moore and P. D. Jennings (Eds.), Human resource management on the Pacific Rim: Institutions, practices, and attitudes: 351-379. Berlin: de Gruyter.

Johnson, W.H.A. 1999. An integrative taxonomy of intellectual capital: Measuring the stock and flow of intellectual capital components in the firm. International Journal of Technology Management, 18(5-8): 562-575.

24

Jones, C., & Hamilton Volpe, E. 2011. Organizational identification: Extending our understanding of social identities through social networks. Journal of Organizational Behavior, 32: 413-434. Kale, P., Singh, H., & Perlmutter, H. 2000. Learning and protection of proprietary assets in strategic

alliances: Building relational capital. Strategic Management Journal, 21: 217-237.

Khanna, M., & Anton, W.R. 2002. Corporate Environmental Management: Regulatory and Market-based Incentives. Land Economics, 78(4), 539-558.

Khanna, T., Gulati, R., & Nohria, N. 1998. The dynamics of learning alliances: competition, cooperation and relative scope. Strategic Management Journal, 19(3):193–210.

Koch, M.J., & McGrath, R.G. 1996. Improving Labour Productivity: Human Resource Management Policies Do Matter. Strategic Management Journal, 17: 335–54.

Koh, H.C., & Boo, E.H.Y. 2001. The link between organizational ethics and job satisfaction: a study of managers in Singapore. Journal of Business Ethics, 29: 309-24.

Koka, B.R., & Prescott, J.E. 2002. Strategic alliances as social capital: A multidimensional view. Strategic Management Journal, 23(9): 795-816.

Kotter, J.E. 1982. The General Management. New York: Free Press.

Kraatz, M. S. 1998. Learning by association? Inter organizational networks and adaptation to environmental change. Academy of Management Journal, 41: 621-643.

Kruse, D. L. 1992. Profit-Sharing and Productivity: Microeconomic Evidence from the United States. Economic Journal, 102: 24–36.

Luthans, F. 1988. Successful vs Effective Real Managers. The Academy of Management Executive, 2(2): 127-132.

Lynch, L.M. 1994. Training and the Private Sector, NBER Comparative Labor Market Series. Chicago and London: University of Chicago Press.

Marsden, P. V. 1990. Network Data and Measurement. Annual Review of Sociology, 16: 435-463.

McWilliams, A., & Siegel, D. S. 2011. Creating and Capturing Value: Strategic Corporate Social Responsibility, Resource-Based Theory, and Sustainable Competitive Advantage. Journal of Management, 37(5): 1480-14-95.

Mohrman, S.A., & Novelli, L. Jr. 1985. Beyond testimonials: learning from a quality circles program. Journal of Occupational Behavior, 6: 93-110.

Moliterno, T.P., & Mahony, D.M. 2010. Network theory of organization: A multilevel approach. Journal of Management, 37: 443-467.

Mowery, D. C., Oxley, J. E., & Silverman, B. S. 1996. Strategic alliances and interfirm knowledge transfer. Strategic Management Journal, 17: 77-91.

Nahapiet, J., & Ghoshal, S. 1998. Social capital, intellectual capital, and the organization advantage. Academy of Management Review, 23: 242–266.

Orlitsky, M., Schmidt, F., & Rynes, S. 2003. Corporate social and financial performance: A meta analysis. Organization Studies, 24: 403-441.

Payne, G.T., Moore, C.B., Griffis, S.E., & Autry, C.W. 2011. Multilevel challenges and opportunities in social capital research. Journal of Management, 37(2): 491–520.

Peterson, D.K. 2004. The Relationship between Perceptions of Corporate Citizenship and Organizational Commitment. Business & Society, 43: 296-319.

Pfeffer, J. 1998. Seven Practices of Successful Organizations. California Management Review, 40: 96– 124.

25

Pfeffer, J., & Langton, N. 1993. The Effect of Wage Dispersion on Satisfaction, Productivity, and Working Collaboratively: Evidence from College and University Faculty. Administrative Science

Quarterly, 38: 382-407.

Ployhart, R. E., & Moliterno, T. P. 2011. Emergence of the human capital resource: A multilevel model. Academy of Management Review, 36(1): 127-150

Porter, M. 1985. Competitive Advantage. New York: Free Press.

Ramus, C.A., & Steger, U. 2000. The roles of supervisory behaviors and environmental policy in

employee ‘ecoinitiatives’ at leadingedge European companies. Academy of Management Journal, 43: 605-626.

Rennison, L.W., & Turcotte, J. 2004. Productivity and Wages: Measuring the Effect of Human Capital and Technology use from Linked Employer-Employee Data. Working paper, Department of Finance, Economic and Fiscal Policy Branch, Canada, No. 2004–01.

Russo, M. V., & Fouts, P.A. 1997. A Resource-based Perspective on Corporate Environmental Performance and Profitability. Academy of Management Journal 40(3): 534-59.

Salis, S., & Williams, A.M. 2010. Knowledge Sharing Through Face-to-Face Communication and Labor Productivity: Evidence from British Workplaces. British Journal of Industrial Relations, 48: 436-459.

Samuelson, P. A., & Nordhaus, W.D. 1989. Economics (13th ed.). New York: McGraw-Hill.

Sharma, S. 2000. Managerial interpretations and organizational context as predictors of corporate choice of environmental strategy. Academy of Management Journal, 43(4): 681-697.

Shook, C.L., Ketchen, D.J, Hult, G.T.M., & Kacmar, K.M. 2004. An assessment of the use of structural equation modeling in strategic management research. Strategic Management Journal, 25: 397-404.

SHRM. 2011. Advancing sustainability; HR’s role. A research report by the Society for Human Resource Management, BSR and Aurosoorya.

http://www.shrm.org/research/surveyfindings/articles/pages/advancingsustainabilityhr%E2%80% 99srole.aspx

Simonin, B.L. 1999. Ambiguity and the process of knowledge transfer in strategic alliances. Strategic Management Journal, 20:595-623.

Skaggs, B.C., & Youndt, M.A. 2004. Strategic positioning, human capital, and performance in service organisations: A customer interaction approach. Strategic Management Journal, 25:85-99. Smitka, M. 1991. Competitive ties: Subcontracting in the Japanese automotive industry. New York:

Columbia University Press.

Sousa-Poza, A., & Ziegler, A. 2003. Asymmetric information about workers' productivity as a cause for inefficient long working hours. Labour Economics, 10: 727-747.

Steiger, J.H. 1990. Structural Model Evaluation and Modification – an Interval Estimation Approach. Multivariate Behavioral Research, 25:173-180.

Stewart, T.A. 1997. Intellectual capital: The new wealth of organization. New York: Bantam Doubleday Dell Publishing Group, Inc.

Tomer, J. F. 1990. Developing world class organization: Investing in organizational capital. Technovation, 10(4): 253–263.

Tucker, L.R., & Lewis, C. 1973. Reliability Coefficient for Maximum Likelihood Factor-Analysis. Psychometrika, 38:1-10

Turban, D.B., & Greening, D.W. 1997. Corporate social performance and organizational attractiveness to prospective employees. Academy of Management Journal, 40: 658-672.

26

Uzzi, B. 1997. Social structure and competition in interfirm networks: The paradox of embeddedness. Administrative Science Quarterly, 42: 35-67.

Viswesvaran, C., Deshpande, S.P., & Joseph, J. 1998. Job satisfaction as a function of top management support for ethical behaviour. Journal of Business Ethics, 17: 365-371.

von Hippel, E. 1988. The Sources of Innovation. New York: Oxford University Press.

Wadhwani, S., & Wall, M. 1990. The Effects of Profit Sharing on Employment, Wages, Stock Returns and Productivity: Evidence from UK Micro Data. Economic Journal, 100 (399): 1-17.

Wright, P. M., & McMahan, G. C. 1992. Theoretical perspectives for strategic human resource management. Journal of Management, 18: 292–320

Wright, P. M., & Snell, S. A. 1998. Toward a unifying framework for exploring fit and flexibility in strategic human resource management. Academy of Management Review, 23(4): 756–772. Youndt, M.A., Subramaniam, M., & Snell, S.A. 2004. Intellectual capital profiles: an examination of

investments and returns. Journal of Management Studies, 41:335-362.

27

28

29

Table 1: Definition of variables and sample statistics

Variable Description Mean S D Min Max

Labor

Productivity****

Valued added per employee in 2008 (ln) 4.13 0.76 -2.37 7.69 Financial

Participation****

Employee profit-sharing scheme (€) in 2008 2475 11,905 0.00 267,038 Interpersonal Relations* Working Relations Working Interaction Helping environment 3.43 2.49 2.02 1.56 1.01 1.30 0.00 0.00 0.00 6.00 4.00 4.00 Inter-organizational Relations* Customer Relation Supplier Relation External Partner Relation

3.56 2.42 1.39 1.88 0.89 1.06 0.00 0.00 0.00 8.00 3.00 3.00 Environmental Practices **

The firm has adopted innovative practices

2.64 2.36 0.00 6.00

Training* Customer Training Quality Training General training 0.56 1.62 2.57 1.47 2.19 2.51 0.00 0.00 0.00 6.00 6.00 6.00

Size*

Number of employees

2506 8569 20.00 111,956Production***

Total Production Sold (€) in 2006

584883 3063321 0.00 392,685, 31 Wage***** Average wage within a firm per hour in2006

15.14 143.01 1.39 10,318

Working hours* Number of working hours per week 37.69 6.96 1.00 84.00

* variables were retrieved from the COI; **variables retrieved from the CIS database; *** variables retrieved from the EAE database; ****variables retrieved from the ESANE database; ***** variables retrieved from the DADS database.

30

Table 2. Measurement paths

Measurement paths Unstandardized

regression weight Standard error Critical ratio Standardized regression weight p-value Interpersonal Relations Working Relations 1.66 0.07 29.88 0.71 ***

Working Interaction 1 (fixed) 0.66

Helping environment 1.00 0.06 29.89 0.51 ***

Inter-organizational Relations

Customer Relation 2.06 0.09 23.97 0.54 ***

Supplier Relation 1 (fixed) 0.55

External Partner Relation 1.43 0.06 25.05 0.66 ***

Training

Customer Training 0.21 0.03 6.70 0.16 ***

Quality Training 0.60 0.06 10.18 0.30 ***

General Training 1 (fixed) 0.44

Notes: *** = p < 0.001.

Table 3. Results of the Structural Model

Antecedent variable Consequent variable Regression weight Standard error Critical ratio p-value Standardized regression weight Hypothesized Relations

Financial Participation Labor Productivity 0.00 0.00 15.89 *** 0.25 Interpersonal Relations Labor Productivity 0.13 0.03 4.23 *** 0.11 Inter-organizational Relations Labor Productivity 0.12 0.04 3.26 0.001 0.07 Environmental Practices Labor Productivity 0.03 0.00 5.89 *** 0.09 Control Relations

Training Labor Productivity5 0.06 0.03 2.31 0.02 0.09

Size Labor Productivity 0.00 0.00 -19.48 *** -0.48

Production Labor Productivity 0.00 0.00 16.93 *** 0.38

Wage Labor Productivity 0.00 0.00 0.99 0.32 0.01

Working Hours Labor Productivity 0.03 0.00 5.89 *** 0.09

31

Appendix A1. Measurement paths (Service Sectors)

Measurement paths Unstandardized regression weight Standard error Critical ratio Standardized regression weight p-value Interpersonal Relations Working Relations 1.62 0.08 21.27 0.73 ***

Working Interaction 1 (fixed) 0.69

Helping environment 0.99 0.05 19.12 0.54 ***

Inter-organizational Relations

Customer Relation 2.05 0.15 13.73 0.50 ***

Supplier Relation 1 (fixed) 0.49

External Partner Relation 1.24 0.09 14.27 0.66 ***

Training

Customer Training 0.69 0.10 6.63 0.33 ***

Quality Training 0.87 0.13 6.86 0.38 ***

General Training 1 (fixed) 0.36

32

Appendix A2. Results of the Structural Model (Service Sector)

Antecedent variable Consequent variable Regression weight Standard error Critical ratio p-value Standardized regression weight Hypothesized Relations

Financial Participation Labor Productivity 0.00 0.00 7.48 *** 0.26 Interpersonal Relations Labor Productivity 0.26 0.04 6.34 *** 0.22 Inter-organizational Relations Labor Productivity 0.18 0.06 2.95 0.003 0.10 Environmental Practices Labor Productivity 0.02 0.01 2.44 0.015 0.05 Control Relations

Training Labor Productivity 0.01 0.04 0.21 0.83 0.01

Size Labor Productivity 0.00 0.00 -11.85 *** -0.42

Production Labor Productivity 0.00 0.00 8.78 *** 0.22

Wage Labor Productivity 0.00 0.00 0.54 0.59 0.01

Working Hours Labor Productivity 0.01 0.00 4.29 *** 0.10

Notes: *** = p < 0.001;

Appendix B2. Measurement paths (Manufacturing Sector)

Measurement paths Unstandardized regression weight Standard error Critical ratio Standardized regression weight p-value Interpersonal Relations Working Relations 1.74 0.09 19.33 0.68 ***

Working Interaction 1 (fixed) 0.62

Helping environment 1.03 0.06 18.24 0.49 ***

Inter-organizational Relations

Customer Relation 2.23 0.11 19.33 0.58 ***

Supplier Relation 1 (fixed) 0.58

External Partner Relation 1.44 0.07 19.61 0.62 ***

Training

Customer Training 0.15 0.03 5.44 0.17 ***

Quality Training 0.55 0.07 7.63 0.28 ***

General Training 1 (fixed) 0.46

33

Appendix B2. Results of the Structural Model (Manufacturing Sector)

Antecedent variable Consequent variable Regression weight Standard error Critical ratio p-value Standardized regression weight Hypothesized Relations

Financial Participation Labor Productivity 0.00 0.00 12.02 *** 0.22 Interpersonal Relations Labor Productivity -0.06 0.04 -1.49 0.14 -0.06 Inter-organizational Relations Labor Productivity 0.08 0.04 1.99 0.047 0.06 Environmental Practices Labor Productivity 0.03 0.01 6.14 *** 0.12 Control Relations

Training Labor Productivity 0.09 0.03 2.72 0.007 0.15

Size Labor Productivity 0.00 0.00 -11.23 *** -0.45

Production Labor Productivity 0.00 0.00 10.58 *** 0.42

Wage Labor Productivity 0.02 0.00 10.53 *** 0.20

Working Hours Labor Productivity -0.01 0.00 -3.69 *** -0.07 Notes: *** = p < 0.001;