Markovian Projection of Stochastic Processes

Texte intégral

Figure

Documents relatifs

The work of Ford, Kac and Mazur [1] suggests the existence of a quantum- mechanical analogue of the Ornstein-Uhlenbeck stochastic process [2]... If in addition

DAY, On the Asymptotic Relation Between Equilibrium Density and Exit Measure in the Exit Problem, Stochastics, Vol. DAY, Recent Progress on the Small Parameters Exit

In order to detail the probabilistic framework in the particular case of the example given in the introduction of this paper, let us consider a component which can be in two

The main result of Section 2 is Theorem 2.3 in which it is shown that the symbolic power algebra of monomial ideal I of codimension 2 which is generically a complete intersection

In the reliability theory, the availability of a component, characterized by non constant failure and repair rates, is obtained, at a given time, thanks to the computation of

The aim of this paper is to prove the exponential ergodicity towards the unique invariant probability measure for some solutions of stochastic differential equations with finite

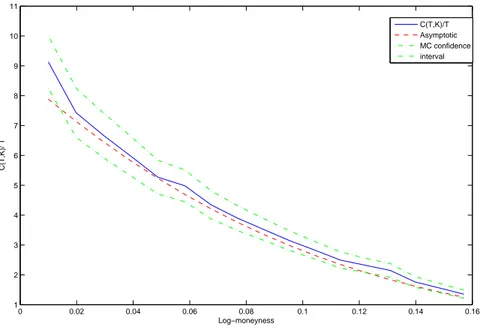

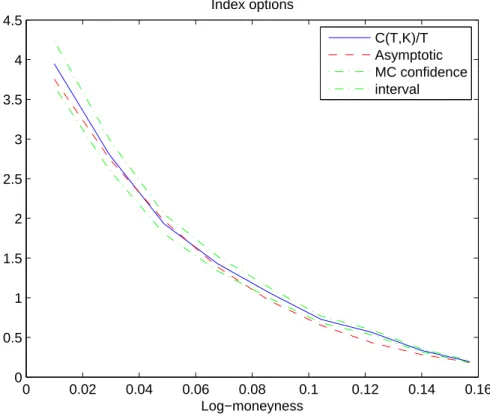

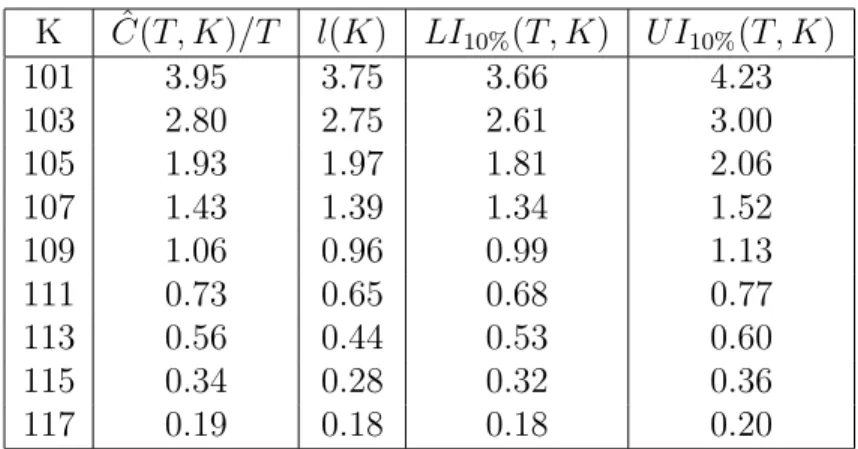

Like in the Brownian case, numerical results show that both recursive marginal quantization methods (with optimal and uniform dispatching) lead to the same price estimates (up to 10

To see how hierarchical and mobile systems may be modelled in this algebra, using the combined sequential and parallel operations, consider a set of automata S and let us denote the