Essais en économie avec frictions financières

Texte intégral

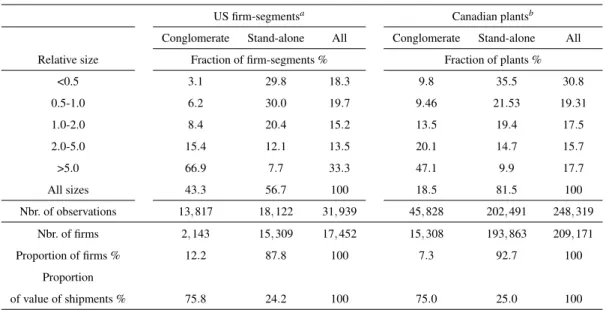

Figure

Documents relatifs

We define a partition of the set of integers k in the range [1, m−1] prime to m into two or three subsets, where one subset consists of those integers k which are < m/2,

Keywords: Behavioural Science, Behavioural Economics, Health Promotion, Public Health, Nudge.. David McDaid is Senior Research Fellow at LSE Health and Social Care and at

Inspired by [MT12], we provide an example of a pure group that does not have the indepen- dence property, whose Fitting subgroup is neither nilpotent nor definable and whose

In those Besov spaces we study performances in terms of generic approx- imation of two classical estimation procedures in both white noise model and density estimation problem..

[1] addresses two main issues: the links between belowground and aboveground plant traits and the links between plant strategies (as defined by these traits) and the

Therefore, the Collatz trivial cycle 1-4-2 (or 1-2 for a compressed sequence) is unique, which solves a half of the Collatz conjecture. Note that a consequence of this demonstration

L’archive ouverte pluridisciplinaire HAL, est destinée au dépôt et à la diffusion de documents scientifiques de niveau recherche, publiés ou non, émanant des