Time Series of Correlated Count Data using Multifractal Process

Texte intégral

Figure

Documents relatifs

(ii) The two linear P-v regimes correspond to dramatically different kinetic modes of GB motion: the linear regime at low driving forces has the characteristic behavior of

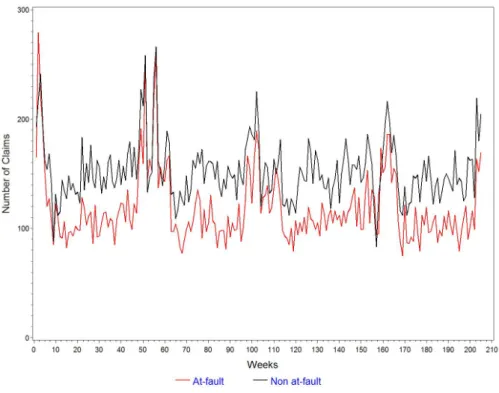

Markov chain but non-homogeneous AR models can reproduce the characteristics of these variations. For example, Figure 6 shows that the fitted model can reproduce both the

Keywords: Markov Switching Vector Autoregressive process, sparsity, penalized likelihood, SCAD, EM algorithm, daily temperature, stochastic weather

Typical sparsification methods use approximate linear dependence conditions to evaluate whether, at each time step n, the new candidate kernel function κ( · , u n ) can be

The second idea which turned out not to be pertinent was generalizing the idea of degree distribu- tion for each simplex order: what is the probability for a vertex to be

Cette enquête a donc permis de collecter des information essentielles pour caractériser les TPE ayant réduit leur durée de travail : comparaison entre celles qui ont

Philippe Esling, Carlos Agon. Time-series data mining.. In almost every scientific field, measurements are performed over time. These observations lead to a collection of organized