Weak approximation of second-order BSDEs

Texte intégral

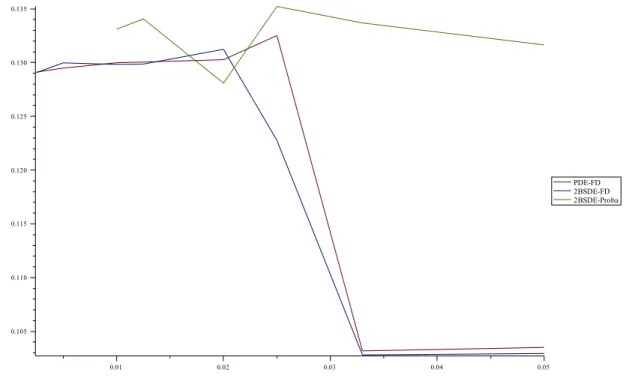

Figure

Documents relatifs

Keywords: incompressible Navier-Stokes equations, vector BGK schemes, flux vector splitting, low Mach number limit, discrete entropy inequality, cell Reynolds number, lattice

A weak second-order split-step method for numerical simulations of stochastic differential

Weak second order multi-revolution composition methods for highly oscillatory stochastic differential equations with additive or multiplicative noise... Weak second

Second order parabolic equations and weak uniqueness of diffusions with discontinuous coefficients.. D OYOON

Indeed, as it has been already said in the introduction, the usual finite element approximation naturally leads to numerical schemes that do not, in general, satisfy the

We study the discrete-time approximation for solutions of quadratic forward back- ward stochastic differential equations (FBSDEs) driven by a Brownian motion and a jump process

[13] Kov´ acs M., Larsson S., Lindgren F., Weak convergence of finite element approximations of linear stochastic evolution equations with additive noise II. Fully discrete schemes,

Renormalization group second order approximation for singularly perturbed nonlinear ordinary differential equations..